Yesterday Education Investor announced that Capita are eyeing the sale of SIMS [paywall]. According to the trade publication:

"Capita will look to sell its education software solutions (ESS) unit for at least £500 million as the listed business services provider’s board this week prepares to approve an auction, EducationInvestor Global can exclusively reveal."(SIMS is the main asset in the ESS division.)

The article contained a range of interesting nuggets, including the fact that ESS generates EBITDA of £50m a year, and that Capita is hoping for a price-to-earnings multiple of 10-14. I hadn't seen a profit number for ESS before: Capita's group 2019 accounts don't provide that level of granularity, but they do report an overall operating adjusted operating profit of £306m on £3.65b of revenue, and the performance of the broader software unit was reported as a profit of £103m on £375m of revenue. The one number we're missing is the percentage of Capita Software's revenue that is generated by ESS, but helpfully this Capita investor presentation gives that as 26% of the total in 2017. So, assuming no significant change in the breakdown since then, it's fair to assume ESS has revenues of c. £100m.

This means we can extrapolate that:

- Capita ESS makes c. £50m of profit on £100m of revenues.

- ESS accounts for under 3% of Capita's revenue (100m / 3670m) and 16% of profits (50m/306m).

- ESS comprises around a quarter of the software unit's revenue (100m / 375m) and almost 50% of its profits (50m / 103m).

In other words, however you look at it, ESS is a cash cow.

So what should we deduce from recent developments? Here are my thoughts.

- Capita think they'll generate more value from selling SIMS than from retaining it. That may sound self-evident, but the numbers are striking. The company thinks they can get £500-700m from the sale. The entire group market capitalisation as I write this is £719m, and the enterprise value (i.e. the company's total value, including debt and suchlike) is somewhere in the region of £2.2bn. So, yeah, I can see how you'd be ok with giving up 16% of profits in return for a fee that equates to 22-32% of your enterprise value, and 70-97% of your market capitalisation. Or, to put it another way, if your group price/earnings ratio is barely above 3, you might be happy to sell one of your bits for a p/e ratio of 10 or more - particularly if you're holding a lot of debt that you'd like to repay.

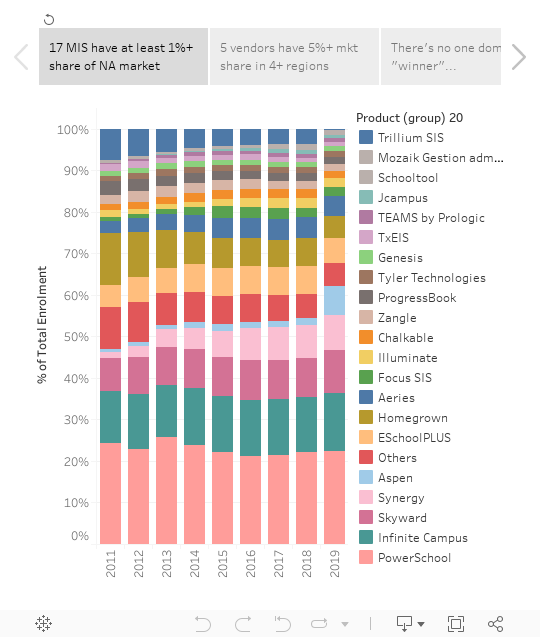

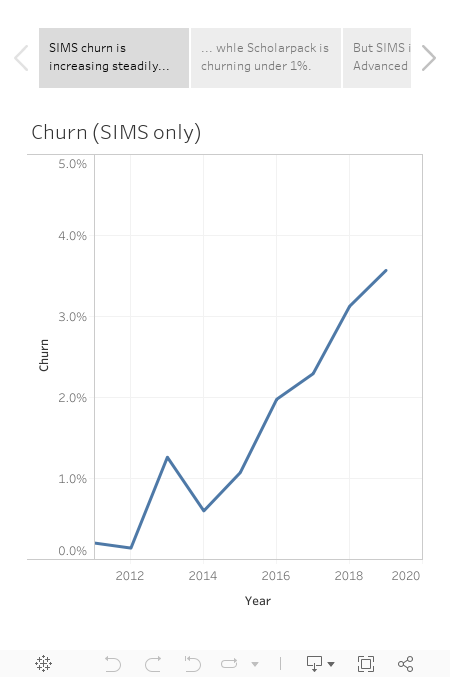

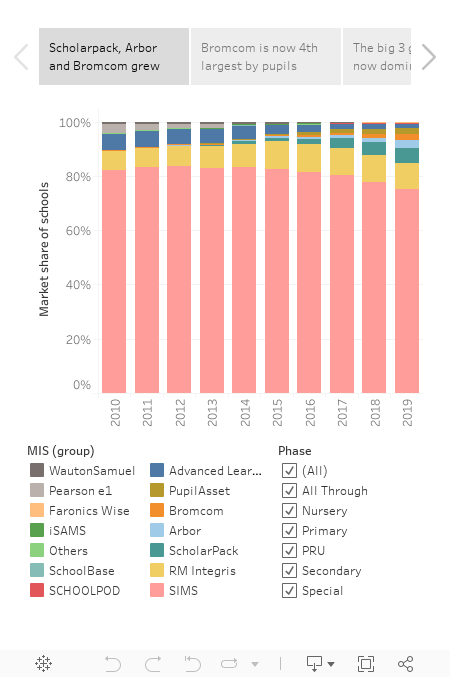

- SIMS' churn may have unsettled Capita. In my blog about 2019 MIS market moves, I included a chart of SIMS churn in English state schools (% of customers leaving year on year). It shows that churn has grown pretty steadily from 0.1% in 2012 to 3.6% in 2019. That's still not anything to be ashamed of, but the result is that SIMS market share when measured by # of English state schools declined from 83% to 75% between 2015 and 2019.

- Capita are happy to let someone else manage the move to the cloud. The main business within ESS is still SIMS 7 - the locally hosted form of SIMS - which has traditionally been sold via local authority support units. Capita have been trying to move SIMS to the cloud for the best part of a decade - first with a pilot project for Northern Ireland that was shelved, and then more recently with the SIMS Primary initiative that was launched at BETT in January 2018. ESS doesn't publish numbers on how many schools have yet made the move to cloud, but we can infer that usage is still very limited from the fact that the SIMS Primary website offers users a chance to register interest to be "the first to know when it's available". The future success of SIMS will of course be bound up in the success of its cloud offering, but clearly Capita are perfectly happy to let someone else manage the headache of how to make the move.

- SIMS' margins may be hard to sustain. However they've managed to price SIMS historically, the key thing to understand margins in the future business is the cloud pricing. And, happily, there is a way of doing just this, since all major MIS vendors now publish a version of their cloud price list on G Cloud, the government's procurement portal. SIMS's cloud offering is still only available for primaries, so let's focus on primary pricing. Using SIMS Primary's G Cloud entry we can see that an average primary of 290 students would pay £4,412 per year for the core software. I calculate the G Cloud cost for comparison of their leading competitors (ScholarPack, Arbor, Bromcom and Pupil Asset) as between £2,370 and £2,865. Now, I should stress, this isn't close to a perfect like-for-like comparison - the range of features included in the list price varies wildly, so the total cost of ownership may be quite different from these headline numbers. But even with those caveats, Capita does look more expensive. That may have been acceptable to customers of the locally hosted product, but in cloud-world SIMS is kind-of the challenger, given the successful cloud businesses that surround them. And with that positioning, they may experience downward pressure on prices from the competition.

- Capita has needed cash. Its competitors don't (yet). Capita's challenges over the past two years were well-publicised, and I'm hardly the right person to add any further commentary. However, what I assume is that as a result, Capita would be keen to generate cash, either by way of profits or selling assets at a good price. At the same time, they're now entering a phase of MIS competition where the competitors appear to be less focused on profitability. Take Arbor (currently the fastest growing challenger) as an example. They recently published accounts, which showed an EBITDA loss of £1.9m (taking into account amortisation, depreciation and exceptionals) on £3.1m of turnover. So maybe an onslaught of investment from competitors makes Capita more open to selling.

- School may not care that much about market rumours... While all this is fun for market watchers, the typical school is unlikely to care that much. One helpful historical defence of SIMS' market share has been how schools procure. Traditionally, the Local Authority entered into contracts with vendors - usually SIMS - and then they (or linked support units) resold licenses to schools. That meant that the typical LA school was unlikely to "go rogue" and buy their own MIS outside the LA's arrangement. Equally, LAs could benefit from the arrangement; support units were at liberty to add a margin on when reselling licenses, and the local support teams were often liked by schools. As a consequence, I'd be surprised if there were many individual schools planning to change their MIS buying decisions based on press rumours about SIMS' parent company. While I like to pore over this stuff on my weekends, the typical school head has better things to do.

- ...However, Multi Academy Trusts and SIMS support units might. These days there are market forces beyond the opinions of LAs and individual schools. First, Multi Academy Trusts (MATs) have become a thing, and they procure differently. Unlike individual schools, increasingly MATs have senior leaders (procurement managers, IT directors, data people and education teams) with the bandwidth and market awareness to run rigorous procurement exercises. Furthermore, challenger vendors have been successful in building functionality that appeals to MATs. That has contributed to a decline in SIMS' market share with MATs (69% in 2019 vs 75% for all English state schools) - and the people who have overseen those switches are more likely to notice ownership uncertainty than stretched staff in individual schools. Then, even the traditional SIMS Support Units are increasingly arms length or standalone businesses, and they may feel unsettled by the potential for change in how their main (and often sole) partner operates. As a consequence, this news may make them more likely to explore other options and start supporting challenger MIS in a way that leads to further choice for schools that are still part of LAs. Mind you, I could also imagine it going the other way: if Support Units have been frustrated about recent developments at Capita (and the slow rollout of cloud SIMS can't have been fun for them) then maybe a sale would seem like a positive development.

Thanks to Ed Tranham of The Assignment Report (great education journalism), Chris Kirk of CJK Associates (high quality education strategy consulting), Nick Finnemore of Finnemore Consulting (equally awesome education product and strategy consulting) and Richard Taylor (legendary education entrepreneur who is never shy around an opinion) for conversations, emails and links that helped me to write this blog.

25/06/20 UPDATE: Since I wrote this piece Capita have released a press release on the planned disposal of ESS, which can be found here.

25/06/20 UPDATE: This blog was edited to consider the enterprise value as well as as the market capitalisation in terms of the potential sales price for SIMS.