Disclaimer: I have past and present commercial relationships with many MIS vendors, including an ongoing involvement with Compass. I'm also a co-founder of two assessment startups - Smartgrade and Carousel - that exist in markets adjacent to the MIS. Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. This matters to me - it's basically the blog I wish had existed back when I was a MAT senior leader trying to get a handle on MIS and edtech. I also now provide MIS market datasets and reports as a service and offer free, informal consultations on MIS procurement to schools and MATs. If you would like to discuss any of this, contact me on Twitter or LinkedIn.

As a startup founder, here's the rough model I use for how to build a successful business:

- Build an innovative minimum viable product.

- Listen to your customers and their suggestions for how to make your good idea into a truly great product.

- Market your company in a way that is warm and appealing to your customers and partners.

- Find the optimal price that allows you to become profitable while also offering great value to your customers.

But it's not the only way! In fact it's not even necessarily the *right* way to run a well-established business, at least from a "maximising shareholder value" perspective. So established companies sometimes adopt very different strategies from startups. Those methodologies may look a bit weird and unfriendly from the outside, but that doesn't mean they're

wrong in terms of profit maximisation. For example,

the owners of 118118 had declining turnover every year in the decade to 2018; but still made a £2.4m profit and withdrew a £64m dividend that year. So sometimes the best way to run a company (from the perspective of shareholders) is to find ways to limit the decline and maximise revenue from the customers that remain. That may not look cuddly to customers, but it might work out just fine financially.

So there was a world where I could be writing this blog and reporting on SIMS declines after a year of

contract tussles and

CMA investigations, and the headline could still be "SIMS will probably be happy with that". My guess is that SIMS has a spreadsheet that was crafted sometime in 2021, and that spreadsheet predicts declines in their market share, while also setting a range for those declines which would be considered acceptable. So to evaluate the past year for SIMS, what we're really trying to do is guess what level of churn they could live with.

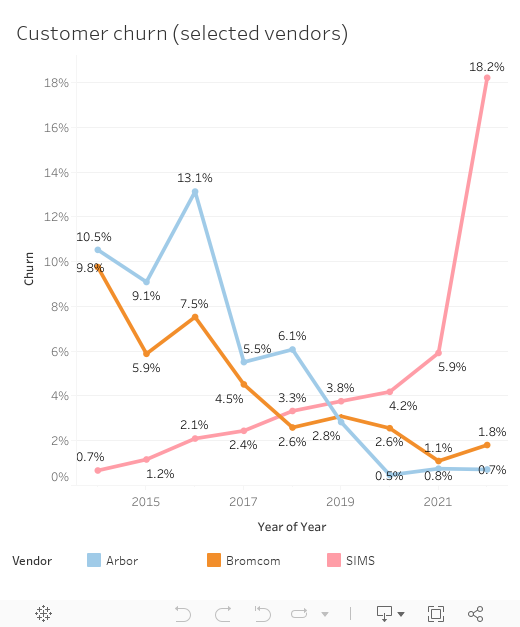

Well, I imagine it was lower than this:

To summarise, over the past year SIMS lost 18% of their market share. 2,734 English state schools took a look at what SIMS was offering and decided to move elsewhere. To put that in context, almost 3 times as many schools left SIMS over the past year compared to the previous 12 months (2022: 2,734; 2021: 942).

The above chart also shows the churn rates for the leading challengers. Both Arbor and Bromcom have churned at under 3% for the past 4 years now, and Arbor has been at under 1% for the past 3 years.

So does this mean SIMS are toast? Well, not necessarily. If you're SIMS you're really hoping that the three year contracts you've enforced mean that at least the the exodus stops now. You're also keeping your fingers crossed that customers will like your new "Next Gen" product once they see it. And you're no doubt cooking up other strategies to keep customers with you.

So in some senses the MIS market data for the next year tells an even more important than this batch of data from the past year. 2022 was about seeing how big the decline was; but we've known for some time that a decline was inevitable. The big question now is: can SIMS stop the bleeding and return to a relatively stable market share? Come back next Christmas to find out!

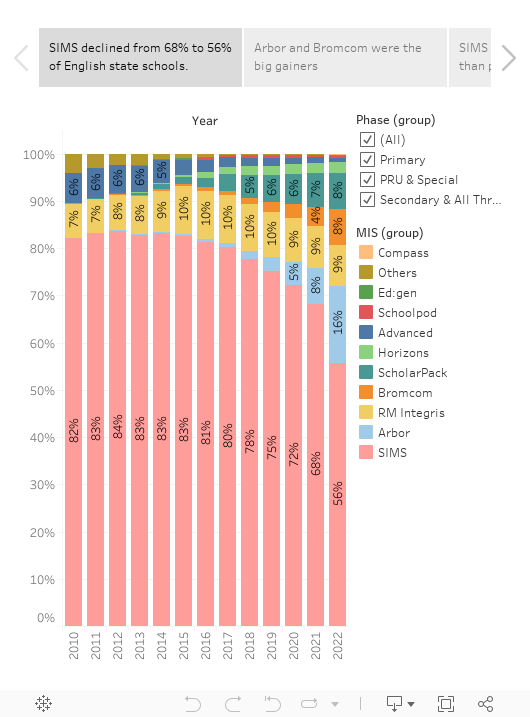

Anyway, SIMS aren't the only story in town, so let's move on to the full market picture. Here are my usual charts showing the latest MIS market share of English state schools.

And here are my key takeaways: