If you've paid any attention to the School Management Information Systems (MIS) market in English state schools over the past decade, you'll know that it moves slowly. Capita SIMS have dominated, with around four fifths of the market, leaving others feeling at times like they're competing for scraps.

However, in the last year or two, there have been signs that things are starting to change. A number of cloud MIS vendors emerged as serious options for schools of all shapes and sizes. This led to 860 schools changing supplier in 2017 (or 4%) of the market; a significant increase on previous years.

So now that

the DfE has released autumn 2018 data, the big question is: is the rate of change picking up?

Well, a first glance at the data suggests the answer is "not yet", with the number of schools switching dropping slightly over the year to 740. HOWEVER, I think that conclusion would be misleading... and so what follows are my three main takeaways from analysing the data, all of which could point to a potentially marked increase in market activity over the coming year.

1) Overall churn hasn't risen, but the most important number has, and by quite a lot.

Churn has never risen above 4% in the past eight years. Or, to put it another way, at most 1 in 25 schools decides to change its MIS in any given year, based on recent trends (see below).

This maddens the challenger MIS vendors, of course. Everyone knows that Capita SIMS has the lion's share of the market, so getting a major foothold requires other to eat into that share. But how can they do that when schools aren't switching?

Well, that brings me to the first intriguing trend (see viz below).

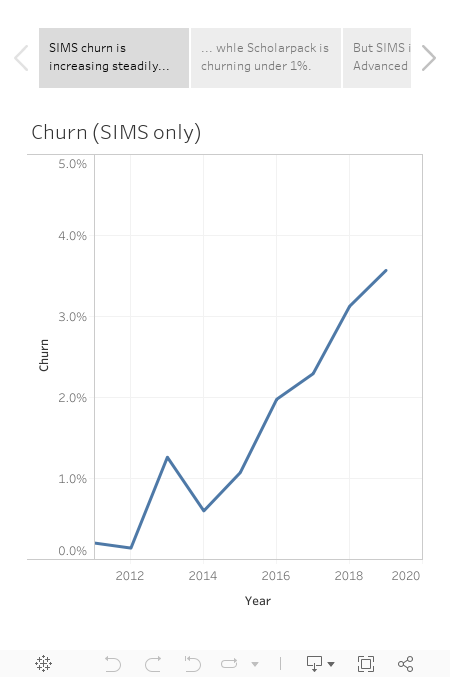

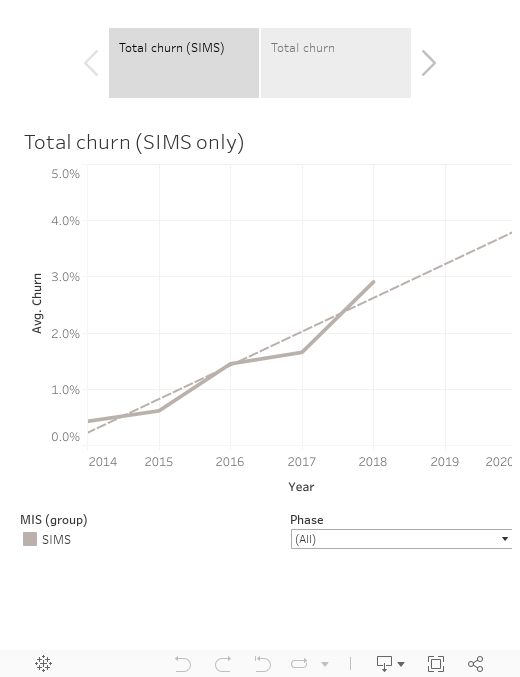

As you'll see from this first viz, The SIMS churn rate has increased for five years straight, from 0.4% in 2014 to 2.9% today. The highest it ever was before this year was 1.7%. And that's for all schools; if you look at primary only, the rate has gone from 0.7% in 2014 to 3.5% today. On current trends, churn from SIMS alone would be 4% of all schools by 2020, and 5% for primaries.

If you click on the other tab on this viz, you'll see the churn for all vendors. What becomes clear here is that until this year, churn was driven primarily by two factors:

- Smaller vendors leaving the market (first Pearson e1, then Wauton Samuel).

- The decline in the share of products owned by Advanced Learning (and Serco before them).

Strip out those one-off changes, however, and there really wasn't much happening, at least until this year. So the rise in SIMS churn will give cheer to the challenger brands. At 2.9% churn, SIMS is certainly not going anywhere; but the others will finally see in this number a real opportunity to compete.

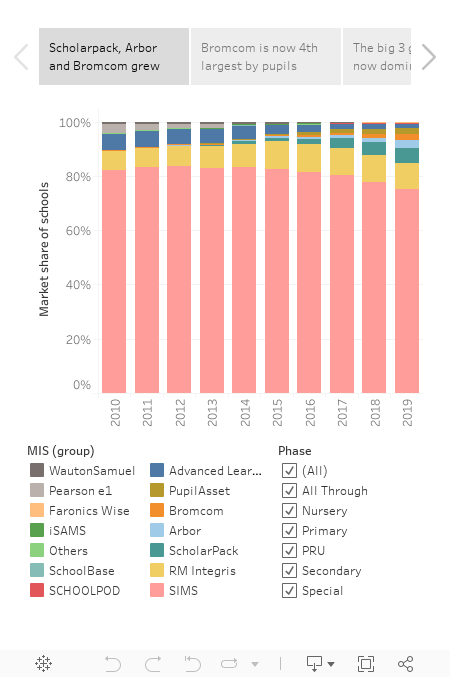

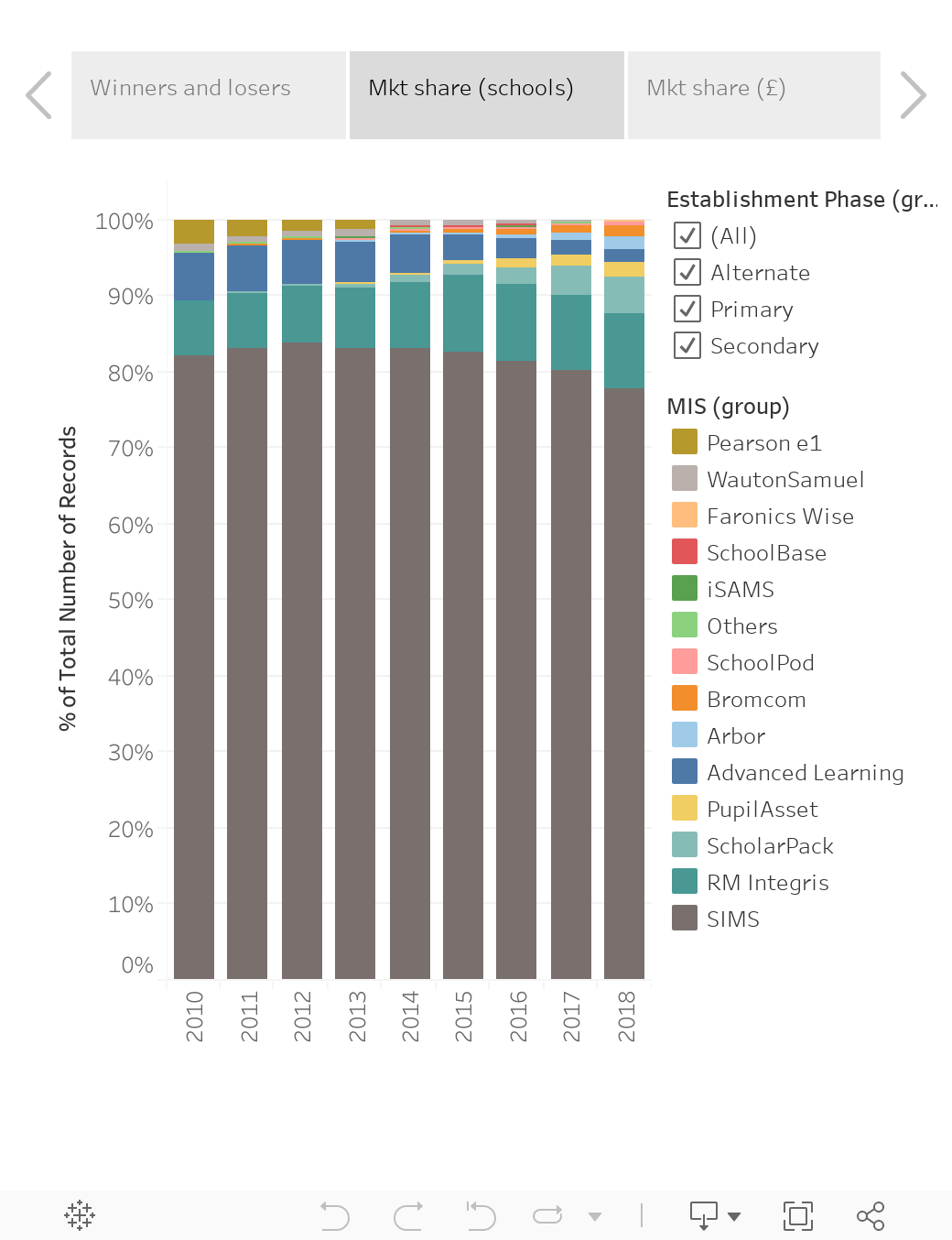

2) There's now a top tier of seven well-established vendors.

In 2010, there were only four notable vendors: SIMS, CMIS (then Serco; now part of Advanced Learning), RM Integris and Pearson e1. There wasn't even a long tail of plucky challengers - Wauton Samuel had a little area of the south east sewn up; but otherwise, that was your lot.

Fast-forward to 2018, however, and you find seven vendors competing for your school's business, and they're all either well established or growing. Those are (in order of market share):

SIMS, RM Integris, ScholarPack, Pupil Asset, Advanced Learning, Arbor and

Bromcom.

In the next viz, as well as listing the wins/losses/market share numbers, I've also included a (very rough) estimate of market share in terms of Annual Recurring Revenue (ARR). What it shows is that these seven are all likely to have ARR of £1m+. I think that's important, as a level of financial strength is required if a product is going to be able to pay for further development and iteration. One other notable insight from the Market share by revenue analysis is Bromcom is a bigger outfit than some give them credit for. This is because their market share skews more towards secondary schools, who typically pay a lot more for their MIS, because of both higher pupil numbers and higher per-pupil pricing, linked to their more complex requirements. By my estimates, Bromcom have c. 2.5% of the total market by revenue, compared to 1.3% by number of schools.

This points to a broader insight, which is that these seven vendors have their own subtle differentiators. As I wrote in

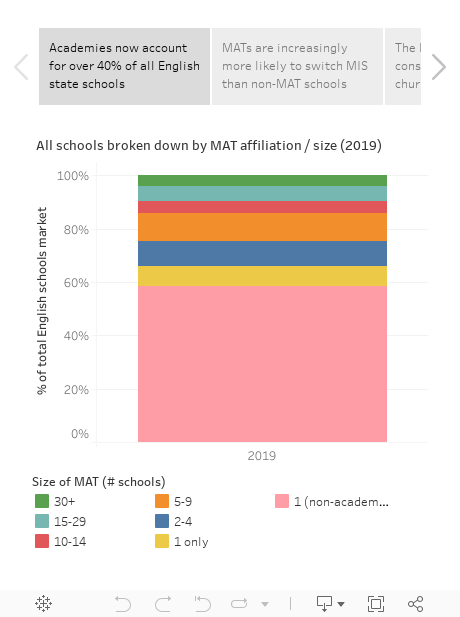

my July 2018 post, MATs continue to dominate among switchers, so their needs are getting a lot of attention. The primary sub-sector is also seeing increased switching, and there's a lot of competition for that business. And for the first time ever, someone other than SIMS won the largest number of switching secondaries: Bromcom gained 40 secondaries in the past year, compared to 33 from SIMS. (A hat tip also to Pupil Asset, Arbor, Advanced, RM Integris and iSAMS, who all added secondaries, albeit in the single digits.)

Finally, an honourable mention goes to

SchoolPod (part of EduSpot), who grew to 131 schools. They are particularly popular with Alternate Provision and Special schools, not all of whom report their census in the conventional way, so it's also quite likely their share is larger (probably also above 1% by number of schools) once that is taken into consideration). So in some ways, it may be fairer to say there are eight notable vendors in the market right now.

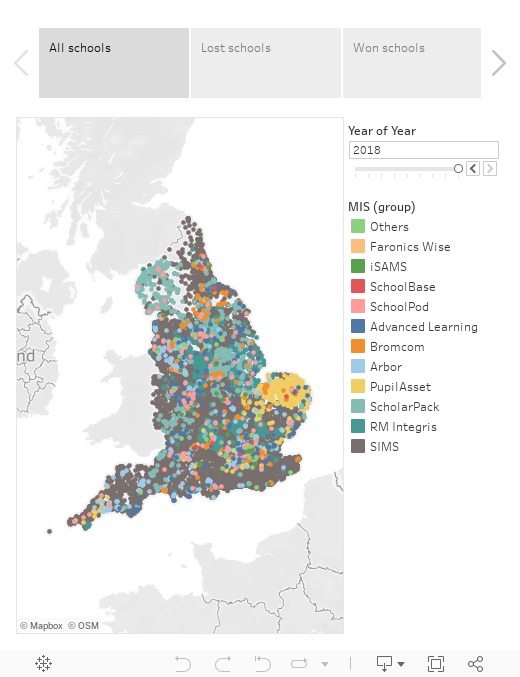

3) Your local schools use a variety of MIS!

A colleague of mine asked me if I could do a viz showing the geographical spread of MIS choice, ideally with a slider so the change over time could be perceived. So I gave it a go, and I'm glad I did, because while playing with the data I spotted a fascinating change.

If you look at the map in the final viz below, and wind back in time from 2018 to 2010, you'll see that the dominance of SIMS is less pronounced in recent years. Then, to understand why this is in more detail, exclude SIMS from the viz. (To do this, choose them from the legend, then select "Exclude"). What jumps out in 2010 is that the challenger vendors each had little toe-holds around the country, but nothing more. Pearson had Norfolk; Wauton Samuel had their South Eastern patch; and Integris and Serco (now Advanced) each had five or six strongholds. That was essentially that. Local Authorities were still the main purchasers, and this led to regional consistency. However, if you then scroll back from 2010 to 2018 with SIMS excluded, what becomes clear is that challenger MIS are now

everywhere.

The growth of MATs has increased the geographic diversity considerably, but more broadly it's also a self-perpetuating trend. In the old days, if you spent your life working in one LA, chances are you'd only know one MIS, regardless of which school you worked at. Nowadays, however, you might have five or six different MIS being used in neighbouring schools. That creates more familiarity with alternatives, and with that comes a willingness to consider options.

So to summarise, the market isn't changing quickly (yet), but it is healthier than it has been for a long time, and the rate of change seems set to increase in coming years.

NOTE: In my day job with Assembly, we're friends and partners of all the major MIS vendors in some way, and we now have deeper commercial partnerships in place with RM Integris and ScholarPack specifically. However, we don't see it as our place to "pick winners" when it comes to school MIS selection, so my aim with this blog is to present data objectively to increase market understanding. I avoid adding anything that could be construed as subjective speculation or opinion.

{kind=link}