But tough luck, because something bonkers happened to me yesterday in just that setting, and it's way more relevant to this blog than you'd imagine. So, if you haven't already, pause your excitement to find out about this year's market stats, check out this Twitter thread, and then come back here to read on....

[...]

Oh good, you're back. That was nuts, right?

Anyway, a brief headline of this year's stats is: yep, SIMS is continuing to decline, but nope, it's not happening as quickly as some vendors and commentators have been claiming.

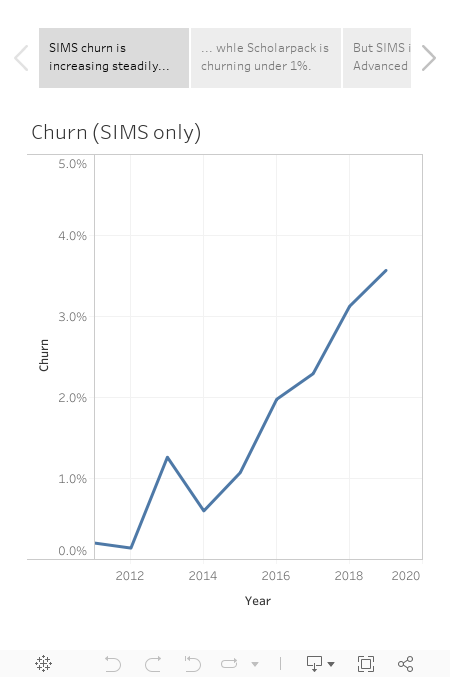

Let's start with churn, since it's frankly the most important metric for understanding the pace of change in the market. Here are three charts that tell you what you need to know (commentary below):

Taking the charts in order:

- SIMS churned 3.6% of its school customers in 18/19, up from 3.1% in 17/18. Bear in mind also that this is the culmination of a steady uptick since 2014, when churn was just 0.6%. That's no doubt cause for concern in SIMS Towers, but given some people have been whispering predictions well in excess of this, it's by no means (yet) a sign of precipitous decline.

- What you can see though, is that the market is inexorably changing in favour of the challenger MIS. The top two vendors (SIMS and RM Integris) churned 3.6% and 4.1% respectively, whereas the third (Scholarpack) is churning at under 1%.

- However, let's not get carried away. The third chart shows Advanced Learning's churn set against that of SIMS. Advanced are something of a parable of what not to do in MIS-land: they have declined from 1,380 schools in 2010 to just 357 today. (Note to self: the story of why that happened is in itself worth a blog someday.) Things looked fine for them in 2011, when they churned just 2.2% - but the canary in the mineshaft came in 2012 when churn jumped to 7%. It rose to over 10% in 2014, and it has been between 10% and 37% ever since.

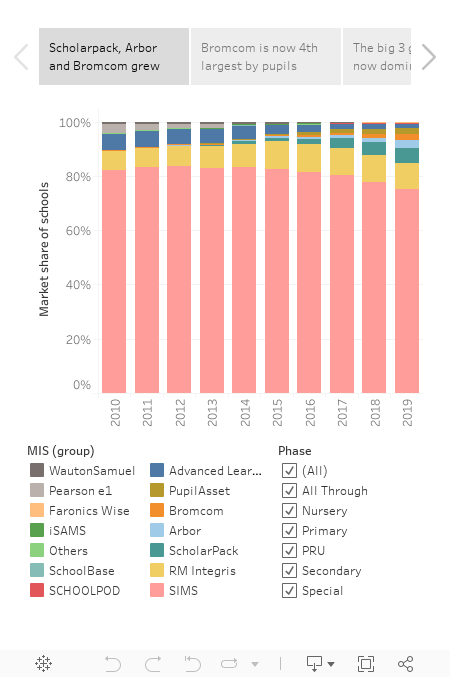

OK, now let's move to the market more broadly. Here are a bunch more graphs (again, with analysis below):

You'll see from these that:

- SIMS market share is now at 75.1%, down from 77.8% last year when measured in terms of the number of school customers. (The decline is smaller than their churn because they won some schools too.)

- RM Integris remains in a clear second place, but also dropped a little (from 2,175 to 2,127 schools), giving further ground to the approaching pack.

- Arbor, Bromcom and Scholarpack all continue to gain, with each being able to claim an important distinction. Arbor grew fastest overall, notching up 277 switchers. Bromcom did best best amongst secondaries for the second year running (which also translates into a greater market share when measured by pupils). And Scholarpack remains the biggest of the three challengers on all measures, with 1,233 schools (5.6% market share by schools; 3.8% by pupils).

- Pupil Asset and Schoolpod stayed solid, without matching the gains of the other challengers. Pupil Asset grew the most, from 410 to 447 schools, and Schoolpod was more or less static at 134 schools vs 131 last year.

- SIMS's losses still are mostly primary-focused, though it's notable that they lost almost twice the number of secondaries in 2019 as they have done in any other year (53, compared to the previous high of 29 in 2018).

- Advanced continue to have a rough time. They gained just 10 schools in the year - the lowest of all MIS who won any schools, and lost 46. They're now the 7th largest MIS in terms of the number of school customers (357 vs 397 in 2018).

- Nobody else is making a dent. iSAMS and SchoolBase held on to their handful of schools (they're both much bigger with private schools, mind), and Faronics are still there with one school customer. But nobody else is making a significant dent on the market, and it'll be jolly hard for anyone else to break in to the market now, given the years of hard work it took Arbor, Bromcom and Scholarpack to build their current momentum.

Right, that's enough for now. I may play around with a bit of additional analysis between now and Christmas, so keep an eye out if you'd like to hear more. Ideas are welcome!

Oh, and I recently left Assembly (my day job until earlier this month), and instead I am now:

- Starting a new schools venture (we're launching in January - watch this space).

- Representing Aircury, an awesome edtech software development agency.

- Doing bits and bobs of advisory work.

A final disclaimer: while I now have a few friends and/or clients who work for MIS vendors, I always aim to write this blog from a neutral perspective. As such, I generally avoid predictions, and instead focus on relating insights derived from the data.