Disclaimer: I have past and present commercial relationships with many MIS vendors, including an ongoing involvement with Compass, an Australia-based MIS that is launching in the UK. I'm also a co-founder of two assessment startups - Smartgrade and Carousel - that exist in markets adjacent to the MIS. Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. This matters to me - it's basically the blog I wish had existed back when I was a MAT senior leader trying to get a handle on MIS and edtech. I also now provide MIS market datasets and reports as a service and offer free, informal consultations on MIS procurement to schools and MATs. If you would like to discuss any of this, contact me on Twitter or LinkedIn.

After buying SIMS in the summer of 2021, new owners ParentPay had some big calls to make. With customers moving to competitors at an increasingly rapid rate, they had to make both technical and commercial decisions:

- Technically, should they persist with SIMS Primary, the pre-existing cloud initiative, or ditch it and build something new from scratch?

- Commercially, how should they present to the market? A charm offensive, perhaps, or discounted pricing to keep schools onside? Or could they find a way to somehow keep schools and raise prices?

Well, as we now know, SIMS chose to:

- Shelve SIMS Primary and replace the project with SIMS Next Gen.

- Move all customers on to 3 year contracts by March 2022*.

- Raise prices (in their own words, by offering "the certainty of a fixed cost for the first year and a capped price increase for years two and three").

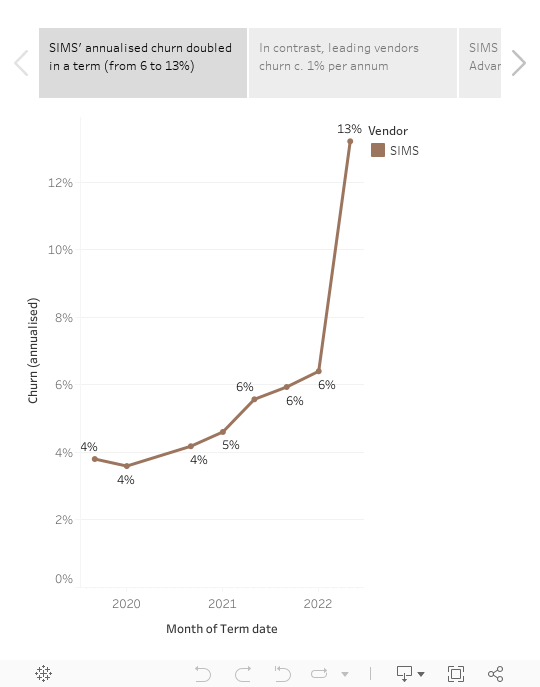

I don't want to get into the ethics of such an approach in this blog, but I do want to reflect on what you might have hoped for if you were the management team behind such a move? SIMS had lost 6% of its schools over the previous year, and so you'd surely be bracing yourselves for an increase on that. It follows that you'd probably bite someone's hand off for 7% churn in the following year? Maybe you'd even take 10% if you felt what you gained in return was valuable enough?

Well, we now have data covering English state schools over the crucial period up to May 2022, and we can see that this is what they got:

As always, these Tableau vizzes are designed to let you explore the data yourself; but here are my reflections having had a proper rummage through:

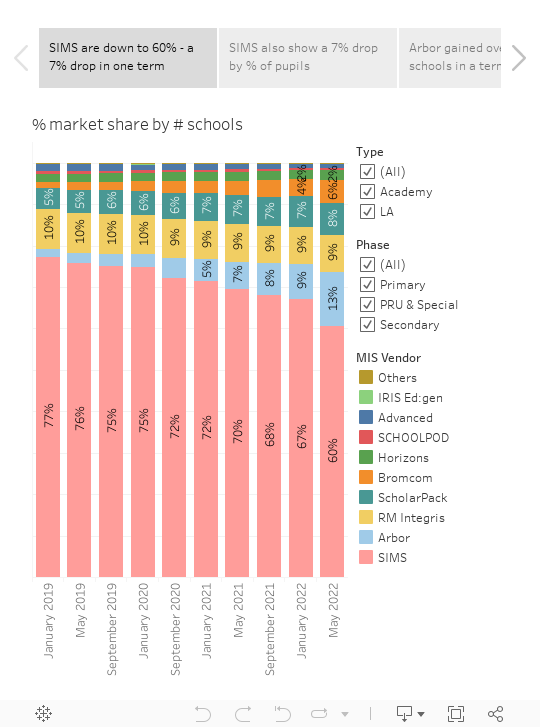

- Arbor remain the leading challenger and are now the second largest vendor overall. Arbor won 1,033 schools in one term, taking their total to 2,913. That's happened less than two years after they passed 1,000 schools in total. They also won the most schools in each of the following categories: primary, secondary, PRU&Special, Academies and LA schools. The performance with LA schools was particularly eye-catching, acquiring 447 schools over the period (the next most was Bromcom with 65), bolstered by their prominent position on the Herts for Learning MIS framework.

- Bromcom are also making big strides. In any other term, Bromcom's numbers would have made them the box office performer. They added 367 schools - more than Arbor has won in any previous term, and similar to the number Bromcom won over the previous five terms combined. And this only includes a handful of the schools they expect to join following their success with the recent West Sussex tender - so we know there's more to come. It's also notable that Bromcom are now the third largest vendor when the market is measured by pupil numbers, with RM Integris dropping down to fourth.

- Other challengers are picking up the pace. IRIS Ed:Gen (a version of iSAMS for state schools) gained 40 schools and Juniper Horizons (a reworked version of Pupil Asset) gained 31. For IRIS the change is particularly noteworthy, since they only started the period with 18 schools.** Both will find reasons to be cheerful in that performance.

- ScholarPack aren't going anywhere either. Given that ScholarPack and Arbor now share an owner (The Key), it's reasonable to speculate as to whether ScholarPack schools will be migrated on to the Arbor platform at some point. Well, the data shows us no sign of that happening yet, with ScholarPack gaining a healthy 93 schools during the term and losing just 2. So it looks like the company is committed to dual-running both products for the time being.

- SIMS are down to a 60% market share. I know I already banged on about SIMS' churn above, but it's worth taking time to acknowledge their overall performance too. Beneath the 60% headline figure, what stood out to me is that SIMS are down to 50% of all academies (you can see this for yourself by using the checkboxes on the first tab of the viz to select academies only). SIMS dropped below a 50% share of large (30+ school) MATs in autumn 2019; and as I've said before, larger MATs lead the way in terms of how smaller MATs behave. I'll dive into the various different MAT size categories in more detail when I look at annual data based on the Autumn 2022 census.

- What to make of RM Integris? I have lost count of how many times I've written a paragraph about Integris that can be summarised as "they didn't lose that many schools, but they didn't really win anything either". If ever there was a term to break that trend, this was it. And you know what...? They didn't lose that many schools, but they didn't really win anything either! 🤷♂️

- Advanced are in serious trouble. As was to be expected after losing the AET contract to Arbor, Advanced dropped from 244 to 186. Their annualised churn is at almost 40%. It's hard to see a way back from here.

- Faronics are gone... I married a Canadian, so I was kind of excited when Vancouver-based Faronics came to the UK in 2018. Well, it's time for me to get un-excited because they're now officially out of the English state school game after their lone school migrated to Bromcom. I'm honestly a bit sad aboot it.

- ... But new names are coming. I was interested to hear SIMS founder Phil Neal big up the ET-AIMS team on a recent fireside chat with Nick Finnemore - so I'd expect to see some schools for them in future updates. And Compass, the Australian MIS I work with, have a healthy pipeline of schools to onboard in the coming months too. When you put those two alongside IRIS, Juniper, Bromcom and Arbor, it means there are now six legitimate growth cloud options. If I was a school procuring an MIS I'd want to take a quick look at all of them before kicking off a procurement exercise - you've got more choice than ever before!

* Schools were subsequently offered a six month break clause, but the broader strategy has essentially remained unchanged.