DISCLAIMER: I have past commercial relationships with a number of MIS vendors. I'm also a co-founder of two assessment ventures - Smartgrade and Carousel - that exist in markets adjacent to the MIS. Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. This matters to me - it's basically the blog I wish had existed back when I was a MAT senior leader trying to get a handle on MIS and edtech. I also now provide MIS market datasets as a service and offer free, informal consultations on MIS procurement to schools and MATs. If you would like to discuss any of this, contact me via Twitter or LinkedIn.

A year ago, reflecting on the news that 18% of SIMS's schools had left them over the previous 12 months, I wrote:

In some senses the MIS market data for the next year tells an even more important than this batch of data from the past year. 2022 was about seeing how big the decline was; but we've known for some time that a decline was inevitable. The big question now is: can SIMS stop the bleeding and return to a relatively stable market share? Come back next Christmas to find out!

I said this for two reasons:

- ParentPay (owners of SIMS) had imposed three year contracts on SIMS customers, at considerable reputational cost, and if all had gone well with the strategy they would have meant that schools became locked in over the past year, stabilising their market share.

- I am a canny storyteller and I wanted to give you a reason to keep coming back for jovial MIS market analysis and pretty data visualisation.

So the news you're all waiting for is: did SIMS stabilise?

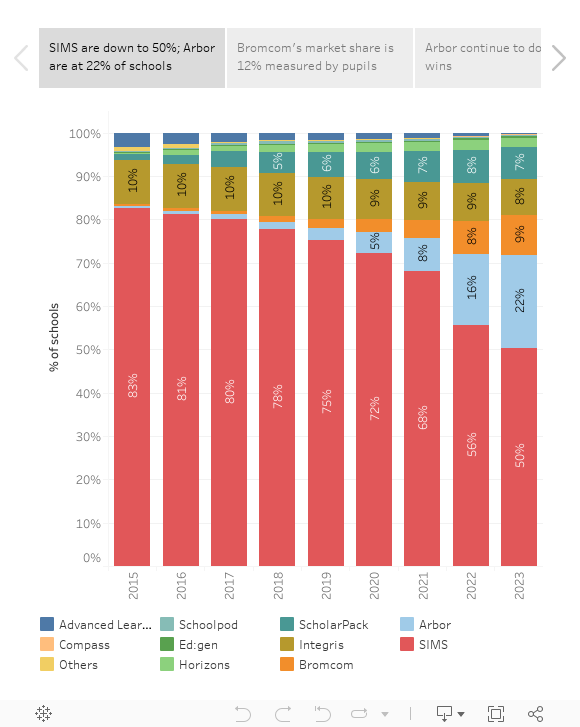

Nope:

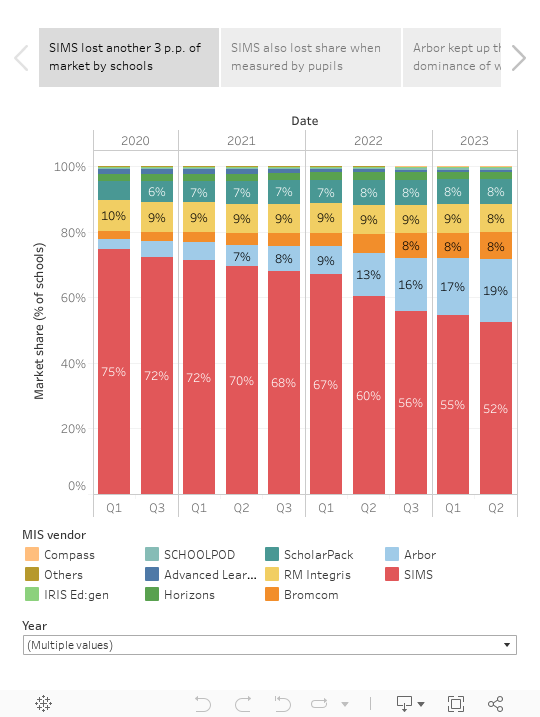

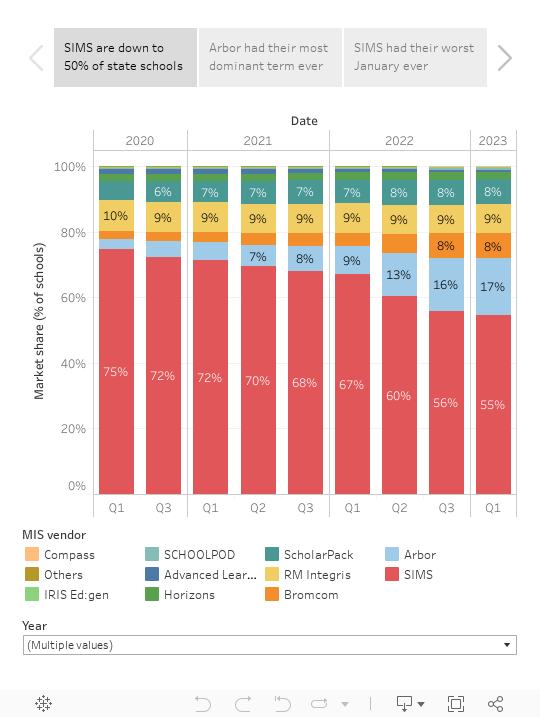

This chart shows the percentage of a vendor's schools that left them over the preceding 12 months. SIMS churned 9.9% of their schools this past year, after losing 18.2% in 2022, taking them down to an overall market share of exactly 50% of English state schools. So while the rate of decline is lower, it's still a major drop compared to any other historical benchmark: healthy MIS generally churn at 2% of less. It's also particularly concerning for SIMS given that their 3 year contract initiative was presumably designed precisely to stop schools switching.

So what's happened? Well, first, the 3 year thing didn't get implemented cleanly - the Competition and Markets Authority (CMA) investigated, and then came to an agreement with SIMS that allowed certain schools to apply for a 12 month break clause, which may have led to a group of delayed switchers. Second, the main MIS challengers all have policies now that mean schools won't pay until their existing MIS agreement ends if they switch while in contract. And third, the SIMS cloud product (Next Gen) is being released module by module, and according to the latest plans it won't be "fully complete" until 2026.

But there's another thing that shouldn't be overlooked: when you're talking to your customers about controversial contract changes, it's hard then to pivot to discussing with them why they should be loyal to you. You see quite a high turnover of staff in edtech account manager roles across the sector, but the people buying MIS may have spent years - even decades - in a MIS commissioning role. What's more, buyers have long memories, and in my experience the stickiest memories are the negative experiences (which is a point that other vendors would also benefit from bearing in mind). So while I've heard some recent noises about the company opening up and softening their messaging, in order to change market perceptions I think they'd need a sustained multi-year charm offensive that helps customers to move beyond the headlines of recent times.

Anyway, there are plenty of stories other than SIMS's decline, so let's get to those shall we? First, here's the data; my analysis of what it shows is below.

- The Key, led by Arbor, now have 37% of all English state schools. Following a year during which The Key completed the purchase of Integris from RM, the company now boasts 3 products with a combined market share of 37%. If the rate of change from the last 12 months continues, The Key will have comfortably more schools than SIMS within two years. Or to put it another way, by 2026 when SIMS Next Gen is a fully fledged cloud MIS, their position as market leader may be a thing of the past.

- Arbor's share of wins in 2022/23 was its best ever. Arbor won 1,212 schools in the past year - 71% of the 1,706 schools who switched. Last year the equivalent number was 61%; before that they were never above 50%. Admittedly, they were helped by 150 or so schools moving from products that are now within the group (i.e. ScholarPack and Integris), but even ignoring those, by my calculations Arbor would have won a record two thirds of switchers. This is, unarguably, a dominant position.

- Bromcom are up to a 12.5% market share when measured by pupils. The only challenger achieving notable growth is Bromcom. They added 368 schools this last year, which would have looked like a chart-topping number in just about any year prior to 2020. What's more, their share of secondaries is just shy of 20%, putting them in second position in this segment ahead of Arbor (16%) and behind SIMS (62%). That's impressive by any standard! All that said, it remains a head-scratcher as to why they're not closer to parity with Arbor. Clearly lots of schools like and trust the system, but I do wonder whether reputational issues linked to their high profile legal action against two MATs continue to hold them back. They did win the case with United Learning - and in fairness to Bromcom it is clear from the judgment that significant mistakes were made during the procurement process - but then again (to quote Schools Week) 'the judge also said that no rule breaches were "deliberate" or in "bad faith".' So if you're a MIS commissioner reading that, are you more likely to see Bromcom as being vindicated, or do you see a business that might come for you if you unwittingly don't get your process right? Or, to put it another way, I feel like a charm offensive could benefit Bromcom too!

- Ed:gen is over 100 schools. When I looked at the termly data from May 2023 there was not much evidence of recent growth for IRIS's Ed:gen, with just 4 schools added in the first two terms of the academic year. But it turns out that didn't tell the real story of their year, because a strong summer took them to 115 schools (2022: 86). Personally I think the 100 school threshold is significant - at that point you've proven that a significant number of schools want what you're offering, and you have an established customer base giving you feedback that helps you to improve your product. Ed:gen also have a notable foothold with secondaries (which is a harder segment to serve than primaries), meaning they're well-placed for further expansion across the board.

- Juniper had a tough year, but it's not all bad news. Juniper's two MIS (Horizons and PupilAsset, which I group together for the purposes of analysis) dropped from 503 to 429 schools. That gives them a higher churn rate than any of the established vendors (15.5%). Obviously that's not the trajectory you want to see as a challenger MIS, though there is some mitigation in the fact that most of the losses link to three largish MAT contracts (Broad Horizons, Diocese of Norwich, White Horse Federation). Set those aside and there were just 12 losses alongside 4 wins. So while Juniper are presumably facing tough competition for their largest MAT contracts, smaller MATs and standalone schools may still be happy enough to hang around. Now clearly that's not nearly as good as demonstrating a growth in the customer base, but it does leave hope that there's a foundation from which to grow if they can improve their go-to-market strategy.

- Compass are up to 7 schools. A year ago, Compass (the Australian HQ-ed MIS) notched their first English school. Since then they've added 6, taking them to 7. So there's some way to go to follow Ed:gen into the 100+ club, but then again, it took Arbor 5 years and Bromcom 7 years to get to that mark. Building a MIS business is a long-term game.

- The Key are starting to consolidate onto one platform. 183 schools left ScholarPack and Integris over the past year, but only 30 of those moved to a competitor; the rest stayed within The Key (mostly moving to Arbor, naturally). I've been keeping an eye out for this kind of managed move since ScholarPack was acquired in 2018, but until this year there was little sign of any formal corporate initiative to consolidate the customer base. I think the caution was wise - you don't want to rush customers to change their MIS until you're confident you can keep them happy during the process - and even now, it doesn't feel like schools are being pushed particularly hard into switching. So taken together with Arbor's low churn (0.4% over the past year), there are signs that The Key will be able to hold on to most of their schools during a possible product rationalisation process.

- Advanced are... still here? 51 schools are still using Advanced products, despite their MIS going end of life in August 2023! 109 did leave them this year though, and interestingly, Ed:gen snagged a healthy 23 of those (Arbor: 46; Bromcom: 30). I guess what this shows you is that while it's hard to win schools, it can also be hard to lose them! No wonder people are fighting hard to enter the market. On which note...

- There's no sign yet of other challengers breaking into the market. Satchel, ET-Aims and Go4Schools have all announced their intentions to sell MIS to English state schools, but they're not showing up in this dataset yet. That's not to say they don't have schools in other markets, or customers piloting modules short of a full MIS, but they're not yet fully fledged MIS vendors.