UPDATED DISCLAIMER: I have past commercial relationships with a number of MIS vendors. I'm also a co-founder of two assessment ventures - Smartgrade and Carousel - that exist in markets adjacent to the MIS. Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. This matters to me - it's basically the blog I wish had existed back when I was a MAT senior leader trying to get a handle on MIS and edtech. I also now provide MIS market datasets as a service and offer free, informal consultations on MIS procurement to schools and MATs. If you would like to discuss any of this, contact me on Twitter or LinkedIn.

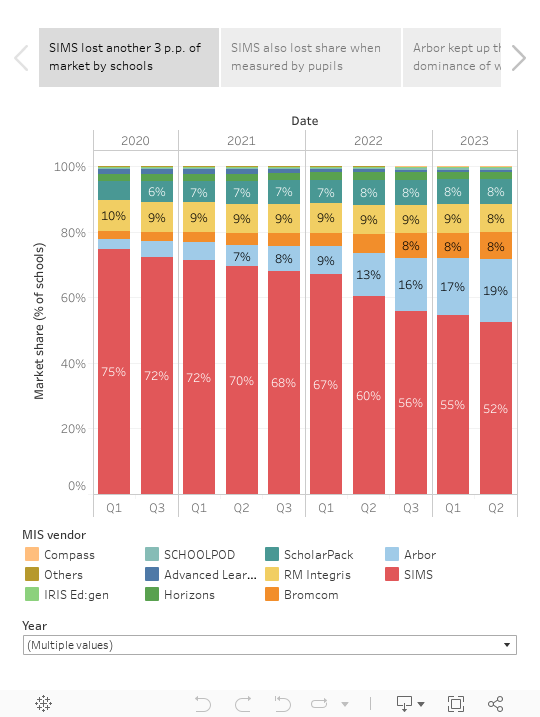

In autumn 2018, SIMS was the chosen school Management Information System (MIS) for 76% of England's state primaries. At that time, Bromcom and Arbor's combined market share was 2%. In the five years since then, we've witnessed the kind of shift that happens rarely in the often slow-moving world of edtech. The summer 2023 data, which I just got my hands on this week, shows that SIMS's market share is now below 50% of primaries for the first time since I've been tracking the market. What's more, The Key (who now own Arbor, ScholarPack and RM Integris) are up to 40% between those three brands. So it's not even really accurate anymore to describe The Key as a challenger: on current trends, The Key will be the largest supplier of MIS to the primary sector within a year.

As always, here are some pretty charts summarising the latest data, followed by a few more observations:

- Arbor is steadily catching up with SIMS. Arbor is up to 4,240 schools overall, compared to 11,545 for SIMS. Nobody else breaks 2,000. They've now been the fastest grower for at least ten terms in a row.

- Bromcom keeps growing too, with 1,851 schools and 11% of the market in the latest data when measured by pupil numbers. They've captured 14% of academies, and they're now up to 4% of LA schools following some notable procurement successes. Arbor remains the faster grower, with over twice the number of schools on its books, but Bromcom is doing a good job of maintaining a growth trajectory, and stands out as the clear third place vendor.

- It was a poor term for the other challengers. I was pleasantly surprised to see IRIS Ed:gen rise from 18 schools to 86 schools during 2022 (incorporating schools still on iSAMS). While they were no doubt helped by SIMS's bummer of a year, that's impressive growth by any standards, and marked them out as a potential breakout candidate in 2023. Well, that hasn't happened yet. In the past two terms, they've added just 4 schools net to be serving 90 schools in total. And things have been even worse for Juniper Horizons, which has 487 school customers (including those still on Pupil Asset), down from 510 at the same time last year. Three terms without growth might be considered something of a warning sign, and I wouldn't be surprised if other MIS are starting to eye up their customer base. In Norfolk, for example, where Juniper have over half of their schools, Horizons/Pupil Asset lost 10 schools in the last year. I'll keep an eye on market share in this LA as it seems like a bellwether for the broader performance of the MIS.

- Compass came from Ireland, and now they're doublin'. As I've mentioned in previous posts, until recently I was an advisor to Compass, the Australia HQ-ed MIS who established a strong presence in Ireland in recent years before winning their first English school in late 2022. In the January 2023 dataset they were up to 4 schools (from 1 the previous term), and that number has now doubled to 8. Compass are the first truly new entrant to the market since Pupil Asset, SchoolPod and iSAMS a decade ago, so they're offering us a fascinating real-time case study in whether it's possible for outside players to break through in England. For a first year in a very competitive market, this is a solid start.

- Plenty of schools are still switching. When SIMS moved to a "3 year lock-in" strategy in late 2021, their hope will presumably have been that after a brief flurry of switching, schools would stick with them on longer contracts while they got a cloud alternative to their core locally-hosted product to market. Yeah, that's not happened, though. Progress is being made with SIMS Next Gen - some primary assessment features were recently announced, for example, but it's some way away from being a finished all-phase product. In the meantime, 601 schools switched MIS between the Spring and Summer 2023 terms, and fully 474 of those were moving away from SIMS. Or to put it another way, more schools left SIMS last term than switched from any system in any full year between 2010 and 2013. I'd say we're on track for 1,300 to 1,600 switchers during the academic year, the majority of which are leaving SIMS.

- Advanced still have 149 schools on their books. Earlier this year Advanced announced that their MIS products were going end of life. So far, only 9 schools have left them this year, meaning that 149 need to find a new MIS home by September 1st. So alongside SIMS leakage, this is another factor keeping the switching market buoyant in 2023.

- Finance is now firmly part of the MIS equation. LAs are increasingly procuring a new finance system at the same time as a MIS. Bromcom have been proudly announcing big LA finance wins. The Key have rebranded RM Finance as Arbor Finance. IRIS is growing a state school MIS business off the back of its popular MAT finance system. So while you clearly can sell a MIS without a finance system, you'll increasingly find yourself in the minority if that's what you're doing.