Disclaimer: I have past and present commercial relationships with many MIS vendors, including an ongoing role as an advisor for Compass. I'm also a co-founder of two assessment startups - Smartgrade and Carousel - that exist in markets adjacent to the MIS. Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. This matters to me - it's basically the blog I wish had existed back when I was a MAT senior leader trying to get a handle on MIS and edtech. I also now provide MIS market datasets and reports as a service and offer free, informal consultations on MIS procurement to schools and MATs. If you would like to discuss any of this, contact me on Twitter or LinkedIn.

I recently got hold of the January 2023 census data. Truthfully, the release at this time of year is never earth-shattering - it tracks schools who move MIS between October and January, and that's just not a super-popular time to switch school systems.

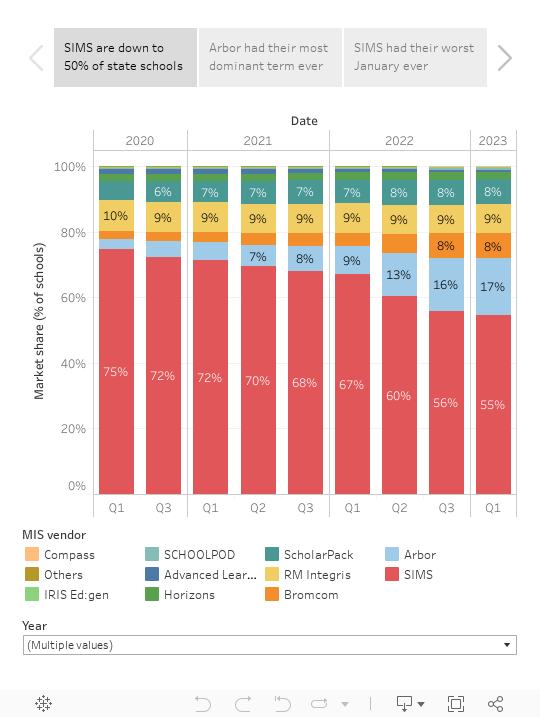

But there were a few things of interest in the numbers, so I'm cranking out a blogpost regardless. As usual, here are the charts, with my analysis below.

- SIMS had their worst winter since (my) records began. SIMS lost 242 schools over the period. That may not sound like much, given they lost over a thousand in each of the preceding two terms, but it's more than they've ever lost over that part of the year since I started tracking things over a decade ago (the next highest was last year, when they lost 228 schools). That's significant, in that it indicates that SIMS's move to 3 year contracts (and associated break clause controversy) hasn't stemmed the tide yet.

- Arbor had their most dominant term ever. 301 schools switched MIS over the period. 236 of those (76%) moved to Arbor. This may in part be because other vendors don't encourage schools to switch over the Christmas period; but still, it's clear that Arbor remain the leading challenger.

- Once the RM Integris acquisition is finalised, The Key will be serving over a third of English state schools. The Key are buying RM Integris, and providing that sale completes following the current CMA investigation then the group will be providing MIS to 34% of the country's state schools. SIMS are at 55%. So I think we can all officially stop referring to SIMS as the dominant market player - there are now two big fish, and only one of them is growing. To misquote the Urban Cookie Collective, they are The Key and they've got the secret.

- Compass grew by 300%. In the autumn census Compass had their first school show up. Well, now they're up to 4, giving them a 300% term-on-term growth rate. If they can keep this kind of growth rate up for the next five years then it is a statistical fact that in 2028 they will be working with over a billion schools. (This is the kind of quality analysis I provide to companies who come to me for advisory services.)

- Spare a thought for Rufford Primary School, the most recent Advanced adopter. Since this data was captured, Advanced have announced that they're shuttering Cloud School this summer. That leaves their 158 schools just two terms to find another home. The news isn't in itself that surprising - the writing was on the wall once their largest customer Academies Enterprise Trust switched to Arbor a year or two ago - but the short timeframes for customers to find a new home is somewhat eyebrow-raising. Which brings me to this blog's "Gah That Sucks" award winners of 2023: Rufford Primary School! Rufford joined Invictus Learning Trust - a MAT-wide Advanced customer - in September 2021, and switched to Advanced last autumn, presumably so that the Trust could have all schools on the same system. So do spare a thought for the poor folks in that school office who trained up on a new system, only to find that they'll have to move to their third MIS in the space of a year by the summer. Ouch.