Disclaimer: I have past and present commercial relationships with many MIS vendors, including an ongoing involvement with Compass, an Australia-based MIS that is launching in the UK Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. This matters to me - it's basically the blog I wish had existed back when I was a MAT MIS commissioner trying to get a handle on all things relating to MIS and edtech. I also now provide MIS market datasets and reports as a service and offer free, informal consultations on MIS procurement to schools and MATs. If you would like to discuss any of this, contact me on Twitter or LinkedIn.

No time for small talk this term - I'm going to get straight to the point. I've just got hold of the latest termly data on the School Management Information Systems (MIS) used by state schools in England. Here are the headlines:

- SIMS dipped below 70% market share when measured by number of schools. I now have eleven years of MIS market data. SIMS' market share peaked in 2012 at 84%. This summer they dropped below 70% (69.6% to be exact). It's higher when measured by pupil numbers (74.6%), but still, the direction continues to be downwards however you cut it.

- 528 schools switched over the past term. That's high by historical standards. We don't have exact data for 2020, because there was no summer census (damn you, COVID, for messing up my beautiful term-by-term dataset), but my educated extrapolation is that the figure for the equivalent period last year was 480-490, and in 2019 the summer term number was 430. That follows a strong number the previous term, which leads me to estimate that there will be c. 1,000-1,050 switchers in the full year to autumn 2021 when we get next term's numbers. That would be a historic high since (my) records began in 2010.

- Wins are still dominated by Arbor, Bromcom and ScholarPack. This isn't news, but there are some interesting subplots to the story. On which note...

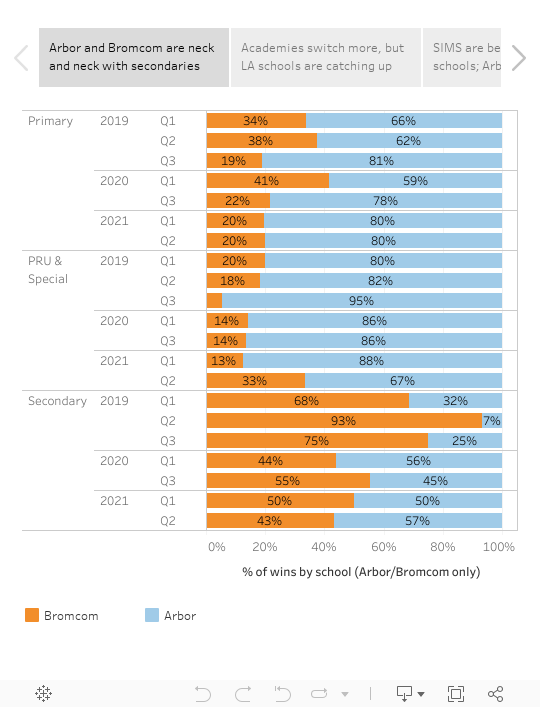

- Arbor and Bromcom are neck and neck with secondary wins. Bromcom remains the dominant challenger with secondaries - they have 299 schools compared to 135 for Arbor. However, Arbor now match them when it comes to new wins. In 2019, Bromcom won four new schools for every school joining Arbor. But over the past term, 29 secondaries joined Arbor, compared to 22 joining Bromcom. Why the change? Well, United Learning had a lot to do with it, accounting for 17 of Arbor's wins. But still, something seems to have changed: over the past four terms, the two have been more or less equally successful with secondaries (Bromcom has 87 wins to Arbor's 84).

- MAT schools are still more likely to switch, but LA schools are catching up. Around 45% of English state schools are academies, but academies (most of which are now in MATs) represent 62% of the switchers. That said, LA schools are increasingly getting in on the switching act: in Q1 of 2018 they represented just 14% of switchers, whereas last term 38% of switchers were LA schools.

- Pupil Asset (now sold as Juniper Horizons) won more schools than SIMS over the past term. It's been a quiet few years for Pupil Asset, so the Juniper team will be heartened to see 25 schools come their way over the past term. That's not at the level of the "big three" challengers, but it was more than SIMS managed to win over the same period (they had 18 wins). Aside from bragging rights for the non-trivial number of ex-SIMS employees now at Juniper, this also points to how SIMS hasn't (yet) found a way of winning schools away from the challengers. Having said that, new owners Montagu have only just had their merger with ParentPay confirmed, and so it feels too early to judge the impact of the new owner's strategy on the long-term prospects of the business.