Disclaimer: I have past and present commercial relationships with many MIS vendors, including an ongoing involvement with Compass, an Australia-based MIS that is launching in the UK Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. This matters to me - it's basically the blog I wish had existed back when I was a MAT MIS commissioner trying to get a handle on all things relating to MIS and edtech. I also now provide MIS market datasets and reports as a service and offer free, informal consultations on MIS procurement to schools and MATs. If you would like to discuss any of this, contact me on Twitter or LinkedIn.

I feel sorry for local news organisations. I grew up in the south west of England, and occasionally stuff happened, but more often that not the local news sounded like:

Something something council business, bla bla squirrels are hurting trees, yadder yadder oh look a royal came to the County Fair...

You get the idea.

Nonetheless, those dutiful regional news teams still had to put out their obligatory half hour of programming, or an unfoldable broadsheet newspaper, or whatever. They had to pretend that everything that they reported on was a big deal. The temptation to arrive on camera and just fess up to the absolute chasmic absence of news must have been overwhelming. "It's 9pm, thanks for joining us, but honestly you really shouldn't have bothered. Make your dinner and come back when Tomorrow's World will be reporting on a curious new invention called the internet." That's the kind of content I'd have respected.

I felt a bit like that when I was preparing this blogpost. Don't get me wrong, there's some good stuff below (e.g. more schools are switching!), but at the same time, if you caught my December 2020 update on the MIS market, you're unlikely to be blown away by the newsiness of it all. Still, you're probably committed to at least a quick skim at this point, so let's get into it.

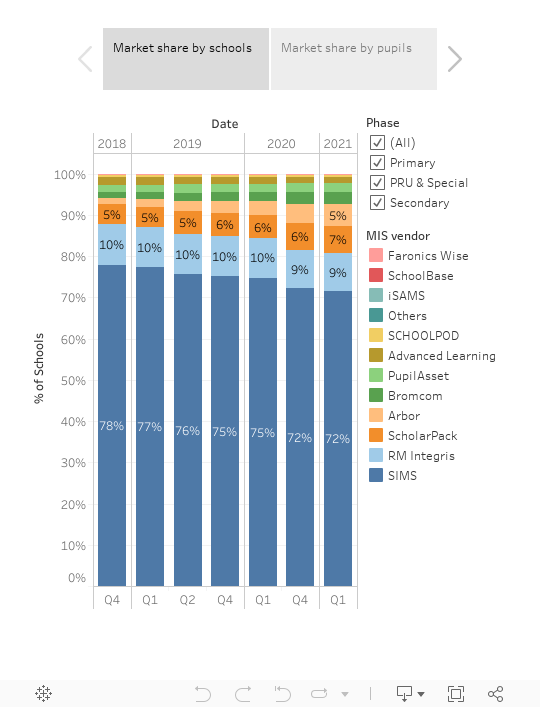

I recently received school MIS market data from January 2021. I've been requesting the termly files for a couple of years now, so I was able to combine it with data stretching back to October 2018 to analyse termly trends. What follows are my five key takeaways, accompanied by some charts, where I think they'll help to emphasise a point.

So, here we go.

1. SIMS churn is at an all time high; challenger churn is at all all-time low

The most important number for all MIS market participants is churn: that is, losses over the past twelve months divided by the number of schools twelve months ago. For established players, you want this to stay low to protect your position. For challengers, you want it to be high.

I've blogged before in my annual blogs about how SIMS churn has grown steadily since 2014 when it was under 1%. The term-by-term data shows this trend continuing. The following chart shows annualised churn using a rolling average of the three previous data periods for the five leading MIS. What you see is:

- Overall churn has been hovering around 4% for a couple of years, and is showing signs of ticking upwards.

- SIMS churn hit 4.5% in Jan 21, the highest rate over the period (and the highest since at least 2010, when my main annual dataset begins).

- There are two clear groups when it comes to churn: the two largest MIS (SIMS and RM), who both churn around 4-5% with churn ticking slowly upward; and the three main challengers (Arbor, Bromcom and ScholarPack), who have been churning at 0-2.5%, with churn ticking notably downwards, particularly in the most recent data set.

That last point is particularly key for those trying to understand where the market is heading. In summary, it's good for challengers! They're keeping their schools while seeing an ever-expanding pool of switchers to fight for. In an ideal world, the challengers would of course love overall churn (which for a while will still mostly mean SIMS churn) to tick up closer to, say 10%. But in the meantime, they can probably live with 4-5% of schools being up for grabs every year, particularly if their own customers staying loyal.

Another way of seeing how churn is changing is to look at the last three years of Oct-Jan switching data only, and compare like-for-like volumes. What you see is that wins are at a three-year high over that period (196 in 2021 vs 191 in 2019 and 145 in 2020). So, while there's no dramatic change, the signs do point to continued growth in switching.

Arbor, Bromcom and ScholarPack continue to be the big 3 MIS in terms of winning over switchers, so there's nothing new there. However, what is new is that Oct 20-Dec 21 was the first period I've ever seen where SIMS was only the fifth best MIS for new wins (Pupil Asset managed to win 5% of schools, compared to 4% for SIMS). Now this could be a blip - SIMS were acquired by Montagu during the period in question - and that kind of transaction is bound to lead to some short-term disruption. Nonetheless, the new management team at SIMS will no doubt be doing all they can to reverse this trend in future periods. Conversely, the Pupil Asset team (who have recently rebranded to Juniper Horizons) will be cheered to see those signs of growth after a comparatively quiet previous year or two.

Another thing to note is that, as with overall market numbers, it makes a difference whether you're looking at schools won, or the number of pupils in schools won. Bromcom won 16% of schools in the period (3rd place for wins), but 25% when measured by pupils (2nd place for wins).

3. Secondaries have (at least) two non-SIMS cloud options.

For at least a year now, Arbor and Bromcom have together accounted for c. 75%+ of secondary switchers, with a fairly even split between the two. That's a significant change from 2019, when SIMS were stronger and Arbor had less success with secondaries.

That's surely good news for schools, who will be increasingly aware that they have (at least) two cloud options.

4. That said, there are plenty of other people trying to shake up the market

Of course, that doesn't mean things won't *ever* change. The last year has seen huge upheaval in the market: as well as The Key buying Arbor, IRIS bought iSAMS and Juniper bought Pupil Asset.

Faronics have been looking to grow a market presence for a few years now, and

Go4Schools also have an embryonic MIS. Keep an eye on

ET-AIMS, which has recently entered the market too. And of course, as I mentioned in my disclaimer, I'm also now helping

Compass (an Australia-based global MIS vendor) to launch in the UK. That's a lot of additional energy being expended on trying to shake up the market...

5. You now have a choice for your MIS market analysis!

What I'm saying is: we're basically now our own sector. Perhaps someone will start a blog to analyse our market share of MIS market page views? And it can surely only be a matter of time before we get our own BETT award category?

Anyway, given this new competitive landscape, I feel the need to provide at least a couple of interactive charts as a thank you for making it all the way to the end. So to close out the blog, here is the full term-by-term picture from Oct 2018 to Jan 2021 (both by school and pupil numbers):