My usual disclaimer: I have past, present and (hopefully) future commercial relationships with many MIS vendors. Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. I also now provide MIS market datasets and reports as a service and offer free, informal consultations on MIS procurement to schools and MATs. If you would like to discuss any of this, contact me on Twitter, LinkedIn or via email.

I made three bold predictions about the MIS earlier this year:

- In January, when talking with a colleague at the BETT Awards, I wagered that one or more MIS would be bought or sold this year.

- Around the same time, I bet a MIS founder that there would be under 1,000 switchers this year; he reckoned it would be over that number.

- In a July blog I went further and said I expected MIS switching volumes to be down on the previous year. That meant I expected under 850 switchers in 2019/20.

So, yeah, I scored a Meatloaf.

Taking those predictions in order, (1) sounds charmingly cautious when reflecting back on the MIS meat market that has been 2020. There have been three major deals, with Arbor, iSAMS and SIMS all changing hands. But still, a win's a win. As for (2), well I win that one as well, but in fairness to the founder, COVID was almost certainly a break on switching. So I'll still smugly claim my pint when this is all over, but he gets the moral victory.

As for (3), I was just plain wrong. As you'll see from what follows, 2019/20 was the biggest switching year since (my) records began in 2010, with 901 schools changing MIS provider. That's newsworthy: it means that even while a pandemic was raging, schools cared sufficiently about their choice of MIS to change their setup. Moreover, the activity wasn't just confined to primaries, where it's relatively well-established now that switching needn't be a hassle; there was more secondary switching activity than ever too.

- There were more switchers than ever before, with 901 schools changing MIS. That just pips 2017, when there were 899 switchers. That's somewhat surprising: like I say, switching was down in the first term of 2019-20, and that was before COVID. That will hearten the new MIS owners, who'll hope for further increases in years to come, particularly as schools with locally hosted MIS reflect on how their lives would have been easier during this dumpster fire of a year if they hadn't had to access a MIS that was hosted in a school server room.

- Arbor is the preferred choice of schools switching MIS. I'm going to give Arbor their own bullet point this year, because they clocked up 413 wins, which is more than any other MIS has managed in a year in the 11 years I have data for. That takes them to 1,065 schools overall - a 1.9 percentage point (p.p.) increase. They were also the clear winner when measuring growth by pupil numbers gaining 1.8 p.p. overall. Bravo, team Arbor!

- Bromcom and ScholarPack also did well. Bromcom grew by 0.8 p.p. when measured by # schools, and by 1.1% when measured by pupils. That matches their growth rate from the previous year, and makes them the third largest vendor by pupil #s with a 4.4% share (behind SIMS and RM). They also won more secondaries than anyone else for the third year running, though Arbor is catching up (2019: Bromcom 57, Arbor 14; 2020: Bromcom 58, Arbor 52.) So hats off to Bromcom too. ScholarPack also have something to cheer: they won 190 schools, taking their market share to 6.4% by number of schools, maintaining their place as the third place vendor when measured by number of schools.

- Nobody else has much to shout about. Pupil Asset has recently been rebranded as Horizons following their sale to Juniper earlier this year, so it's perhaps understandable that their market share stayed flat at 2%. They'll be hoping for better days in the coming year: their strategy of combining a MIS business with their leading position in the primary tracker market needs to start bearing fruit to justify the considerable investment being made. RM Integris dropped a bit for the fourth year in a row (2019: 9.7%; 2020: 9.2%), which will be cause for considerable head-scratching in their Oxfordshire office. They're the vendor I find hardest to get a handle on: there's nothing disastrously wrong, but somehow they can't translate their position as the largest cloud vendor into a growing business. Advanced slipped back again (2019: 1.6%; 2020: 1.5%), and honestly it's hard to see any signs for cheer for them, given the dramatic declines they've suffered since they had an 8% share a decade ago. And SchoolPod have stagnated at 0.6%, so there's not much to report on there.

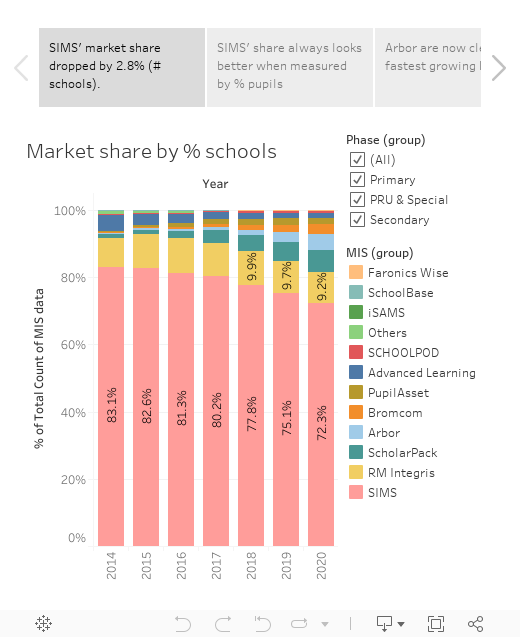

- SIMS continues to slide, with its market share down to 72.3% (from 75.1% in 2019) when measured by number of schools. Most concerning for imminent owners Montagu will be a record number of losses overall (692), with a notable rise in secondary losses too (2020: 90; 2019: 58; 2018: 36). That's not ideal for the new parents - while SIMS has been losing market share at primary for some years, the hope has been that the secondary business would be more resilient. This will only add to the urgency to get good SIMS cloud products out there for all phases, but of course that's no small feat.

- The Key is now the second largest vendor, with a combined 11.2% market share when measured by number of schools, leapfrogging RM, who have 9.2%. They're also the biggest by # pupils (8.3% compared to 6.4% for RM).

- Larger MATs are the most eager to move away from SIMS. In 2014, 79% of schools now in the largest MATs (30+ schools) used SIMS. Just 41% of those same schools now do so. While the declines are slightly less pronounced in other MAT size categories, they're still meaningful, and SIMS has just 63% of the MAT market overall when measured by school numbers (down from 84% in 2014). As I blogged about earlier in the week, SIMS needs a new MAT strategy, and fast.

Now I love a nice, snug trend line, and they don't get much snugger than that! For six years, SIMS' churn rate has increased inexorably, and if things continue on that trajectory they'll be churning 5%+ in a year's time. This will no doubt concern the incumbents and cheer the challengers: in many ways, SIMS churn is THE important number, since the market can't meaningfully move without SIMS giving up schools to the competition.