Disclaimer: I have past, present and (hopefully) future commercial relationships with most of the UK's MIS vendors. Nonetheless I aim to write this blog impartially, from the perspective of a neutral observer. If you have questions about this analysis, or any other blog, contact me on Twitter, LinkedIn or via email. I also now provide MIS market datasets and reports as a service - get in touch for more info.

It's been a pretty hectic few months for MIS market watchers. First Pupil Asset were sold to Juniper Education; then Capita announced it was putting its Education Software division (i.e. SIMS and a few other bits and bobs) up for sale. So, with plenty of people having reason to keep an eye on the market, I decided to take a look at the Jan 2020 English State School MIS census data.

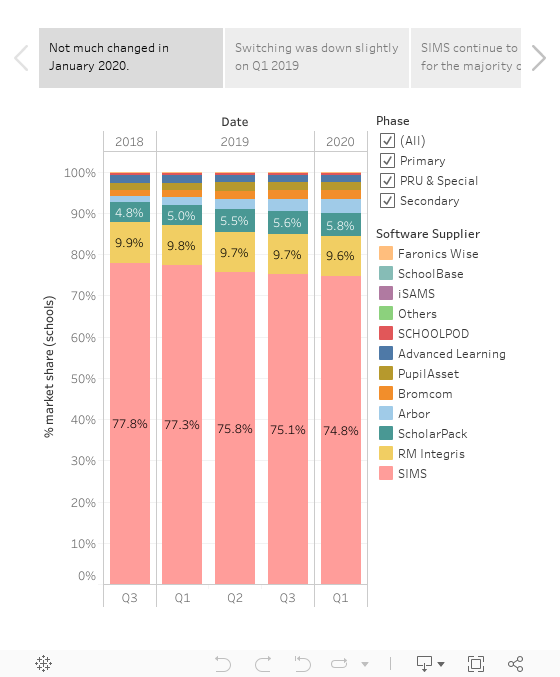

And the news is... underwhelming. The headline is that only 140 schools switched MIS between October 2019 and Jan 2020. Given that over 800 schools changed MIS over the twelve months preceding that period, that's nothing to shout about.

To understand this number in a historical context, I decided to put together a term-on-term dataset. I only started collecting and cleaning termly (as opposed to annual) data in Sep 2018, so I have five terms of data to play with. Here are a few vizzes from that dataset, followed by my conclusions:

- Switching is slightly down on 2018-19. 180 schools switched between October 2018 and January 2019 compared to 140 between October 2019 and January 2020. In other words, compared to the corresponding period in the previous year, switching is down. That said, the autumn-spring period was also the lowest-volume period last year, so the reduction could be linked to the fact that schools don't particularly want to switch MIS over the autumn term / Christmas break. Still, when you consider the fact COVID is likely to lead some schools to postpone system changes between the spring and autumn terms of this year, I think it's a fairly safe bet that switching will be down in 2019-20, compared to the previous academic year.

- SIMS didn't lose much ground over the past term. SIMS' market share dropped from 75.1% to 74.8%. That's hardly an earth shattering decline, but nor is it a sign of market share stabilising. Given recent trends, the limited losses may count as good news for Capita as they prepare the business for sale.

- Bromcom, Arbor and ScholarPack have emerged as the three leading challengers. 86% of the switchers over the term were won by Arbor (39%), Bromcom (24%) and ScholarPack (23%). Those numbers track pretty closely with the average over the four terms I examined (Arbor 35%; Bromcom 21%; ScholarPack 21%). I think it's fair to say these three are now the leading challengers, because...

- Pupil Asset's growth has stalled. In the past term, Pupil Asset gained just one school. In each of the three previous terms they had low double-digit wins. That may be a concern for their new owners, who will no doubt have high hopes for their new acquisition. Mind you, they only lost 2 schools over the past term, and over the four quarters they lost just 10 schools, which is fewer than any of the other notable challengers (ScholarPack 11; Bromcom 12; Arbor 14; SchoolPod 18; Advanced 62; RM 120). So it would seem that their existing customers are happy enough to stick with them; the challenge for Juniper now is to work out how to persuade other schools to switch to them.

- The Advanced turnaround hasn't started yet. Advanced won no schools over the period, while losing 11. I understand that there is considerable effort and investment going into reversing Advanced's decline, but it isn't translating into new business yet.

- RM Integris continues to be... fine? Integris is always a weird MIS to write about. They remain the clear second-place vendor in terms of market share by schools (9.6%), and unlike SIMS, their product is cloud-based and has been for some time. So you'd think there'd be some sort of growth story in their numbers... but there just isn't. Alongside 4 wins, Integris lost 24 over the past term, bringing total losses to 120 over the four-term period. Their market share looks pretty stable; but while other vendors have found a winning formula to nibble away at SIMS' share, RM are actually dropping ever so slightly.

A final word on data validation: for those of you who look really closely at the numbers, you'll notice that the switching totals for prior periods are slightly different than those given in previous blogs. That's mostly because I've come up with some new techniques for identifying schools that switched during or after academisation. At that point, schools get issued with new unique codes, so you need to do some jiggery pokery if you want to match the "old" and "new" school records over time. It's also partly because all schools in Bournemouth and Poole changed their "LA" codes a couple of years ago, and since I rely on those codes to work out who switched, I needed to do some file cleansing to spot switchers in that area. Which leads to my final observation of the blog, which is that writing about MIS has turned me into someone who likes to gossip about changes in LA codes. What have I become?