Arbor announced today that they had won the tender by United Learning (UL) for a Management Information System.

Why is this a big deal? Well…

- UL is the biggest MAT. With 72 state schools, they’re by some distance the biggest MAT. With only 21 MATs having more than 30 schools, this makes them one of the clear “crown jewels" of the sector.

- UL are everywhere. That means the surrounding areas of schools from Carlisle to Kent will have an alternative in their area. If you believe that awareness is one of the main issues holding schools back from switching then deals like this help to bring alternatives to the attention of other heads in the areas surrounding the switching schools.

- It was an an open and EU-compliant competitive process. Not to cast aspersions about other MIS tendering processes, but not all schools / LAs / MATs run the most rigorous processes. United Learning went "full-OJEU" (i.e. they ran a competitive and open process), which means they’ll have needed to be careful and methodical in their approach. It therefore follows that the winner can feel proud of having won in a fair fight. On which note...

- It cements Arbor’s position as the fastest growing challenger. It has become increasingly apparent in recent times that there are three main challengers to SIMS: Arbor, Bromcom, and ScholarPack. For at least four terms in a row now, Arbor has been the fastest growing of that pack - but Bromcom have been particularly successful with large, mixed-phase MATs (Ark, Harris, Oasis, David Ross and Hamwic are all customers). So this win will help Arbor to position themselves as a strong large-MAT option. (NB: ScholarPack are primary only, so wouldn’t have been in the running in this case.)

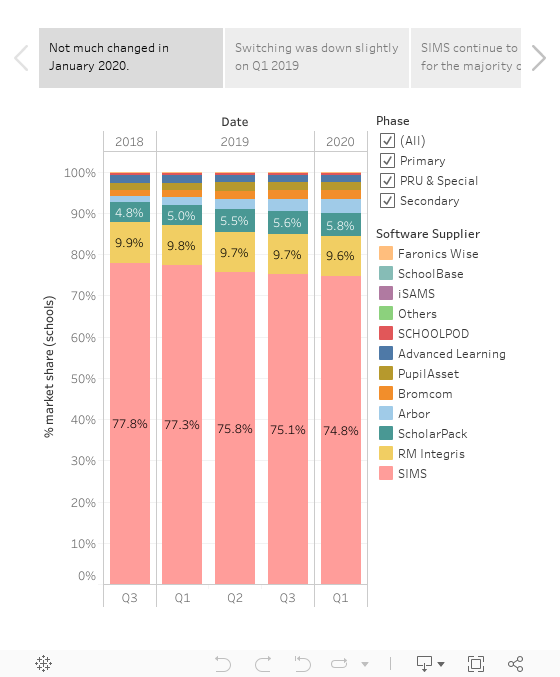

- It emphasises how SIMS is struggling with larger MATs. SIMS were already down to 48% of large (30+ school) MATs in Autumn 2019. Since then, Hamwic have announced a move to Bromcom, and now UL are moving to Arbor. Those changes alone will reduce SIMS down to a 39% share of large MATs by # of school (assuming no offsetting gains), with Arbor and Bromcom both having solid double-digit shares of this subsector. SIMS keep the plurality, but perhaps not for that much longer. So, if you believe that large MATs lead the way in how smaller MATs behave, this is a trend that could have a ripple effect for years to come.

- SIMS aren't winning over large MATs with their cloud proposition (yet). This tender was explicitly for a cloud MIS. So if SIMS bid, they did so based on their cloud offer. The fact they didn't win means they aren't yet succeeding on that front, at least with more complex MATs. It also is another nod to the fact that MATs really care about the benefits that cloud can offer around security/resilience/value: UL weren't willing to consider a MIS that wasn't in the cloud.

- MATs can still procure during COVID. UL started this process in 2019, but you'd have forgiven them for pausing things because of COVID. But clearly the trust doesn't see any issues with ploughing ahead in spite of the pandemic. Other MATs looking on may well think "well, if a a 72 school trust can do it, we can too."