Anyway, when I'm not blogging or leading my ventures, I provide MIS market consulting and data to investors, and offer free, informal consultations on MIS procurement and assessment strategy to MATs. If you would like to discuss any of this, contact me via LinkedIn.

There are basically two types of readers of this blog:

- People who want to know the latest data on the English state school MIS market, because it's in some way relevant to their job.

- People who have at most a tangential interest in MIS, but who enjoy niche puns and arcane musical references.

This Christmas, I'm feeling whimsical, and so I'm going to pander to the second group. But before I get into it, I just want to apologise to you if you're in group 1. Typically the members of this tribe are busy people: investors in edtech for example, or overworked data managers. The kind of people who are right now wondering if it's really too much to ask for hard data unadorned with silliness. So if that's you, I can only apologise in advance.

If you're in group 2 however, I have excellent news, because this Christmas, I'm telling you the story of the latest MIS market data through song titles. First, as always, you get a pretty set of charts, followed by nine tunes that attempt to capture What's Going On.

1. A Change Is Gonna Come

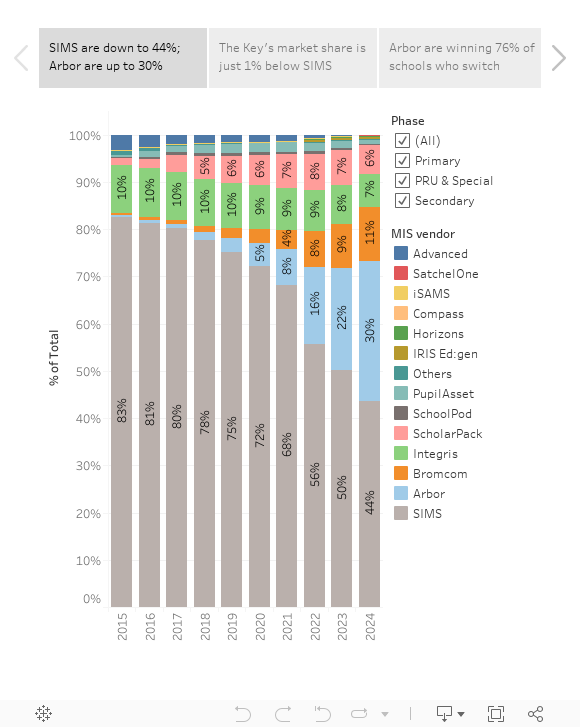

Every time I write this blog I need to find new ways to say Arbor / The Key are bossing the MIS market. Arbor now sit at over 6,500 schools, and perhaps even more notably, if you tot up all schools purchasing a MIS from The Key (i.e. customers of Arbor, Integris and ScholarPack) you get 9,444 schools in total - just 142 short of the SIMS total! That means that barring a remarkable turnaround in fortunes, the next time I blog I'm going to be talking about The Key as the English state school market leader. They also keep broadening their offer: earlier this year they announced the acquisition of FEPS, providers of HR software and services, offering an indication that they see this as a strategic area for future growth.

Now, to be fair, The Key's seemingly imminent coronation as market leaders is only the case if you're measuring the market by number of schools. If you instead consider market share in terms of the number of pupils at the schools served by vendors, SIMS is on 47%, vs 36% for The Key. On this measure, Bromcom also do better, with their share shaking out at 15% by pupils vs 11% by number of schools. So perhaps a more accurate (but less snappy) title for this blog would be: "A Change Is Gonna Come, Or Isn't, Depending On The Metric You Use".

2. Half Yourself? A Merry Little Christmas.

In 2014, by my records, SIMS served 18,247 English state schools. In the latest data, they're at 9,586. So not quite half yet... but close.

What's more, by my calculations they've lost a little under 1,500 schools in the past year, up from around 1,200 in the previous year. SIMS only need to lose another 500 or so schools to have fewer than half the schools of their 2014 peak. If current trends hold, that'll happen within the next six months.

Now, that doesn't mean SIMS is doomed, of course. Trends can change, and the SIMS team are busy developing SIMS Next Gen, which they describe as "The best cloud MIS in education". The roadmap is available online, and it shows all modules being ready by the end of 2026. So I guess a lot depends on how their remaining customers - and future prospective customers - view this product, and it's certainly too soon to come to a verdict on that based on data alone.

But, as befits the song title of this section, let's be Frank: the loss of 13.5% of the customer base from the previous year does not yet indicate any form of renaissance yet. Moreover, there are other considerations that could foreshadow another difficult year ahead. Reportedly, lots of SIMS schools are on 3 year contracts which started in April 2022, meaning 2025 will bring about those schools' first chance to exit their agreements for some time. The big question for SIMS is therefore how many of these can they hold on to? I'll have data on that in summer 2025, so we'll know soon enough!

3. You Win Again.

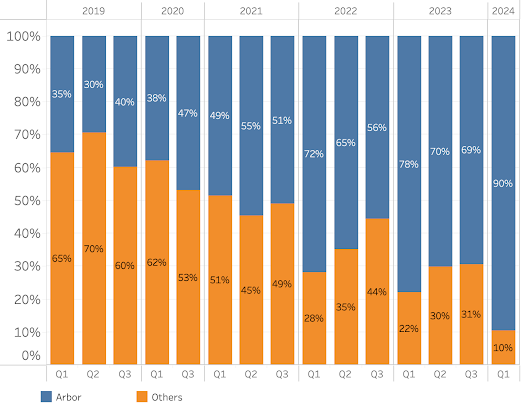

The metric I always use to work out who's winning is what percentage of all switching schools schools did each vendor win? And for Arbor, the rate is 76%; (their best ever),. The savvy among you may wonder if this is artificially boosted by schools switching from other products owned by The Key, but I looked into that, and even if you remove those they're winning 73%.

That's the sixth year in a row that Arbor have had the highest win % amongst vendors, and the fourth in a row where they've been over 50%. Truly, all they do is win win win no matter what what what.

4. Belfast Child.

The English state school numbers don't always do Bromcom full justice. Sure, they're by some distance the next fastest growing MIS after Arbor, with around 2,500 schools in this segment of the market and a decent enough win rate of 21%. But the Simple Minds who look at those details along will assume they're forever in Arbor's shadow - and they'd be wong.

That's because the biggest story of the past year for this company is how they've fared outside England. In January 2024, the Northern Ireland Education Authority announced that Bromcom had won a contract to provide a MIS to their 1,100 schools. Yep, Bromcom won a whole country!

They've also made some important gains in Wales, with Wrexham announcing that they're moving wholesale to Bromcom. Surely it can only be a matter of time before renowned actor and Wrexham AFC owner Ryan Reynolds rocks up at BETT on the Bromcom stand? And with most other Welsh LAs still being on SIMS, Bromcom will be doing all they can to make further inroads west of Hereford.

One other interesting nugget about Bromcom is that they do best in England with large MATs. For groups with 25+ schools, Bromcom has a 30% market share, vs 39% for Arbor and 21% for SIMS. This reinforces the perception that they're most likely to win when the procurement exercise is bigger and more complex.

5. In Between Days.

It's hard to know what to say about IRIS. On the one hand, they're now a bona fide challenger MIS. They've had 100+ schools for over a year, and that's my benchmark for when a vendor has properly become established in the market. They're also still growing, so things are going in the right direction.

That said, the pace of growth in the past year is likely lower than they'd have wanted. They're now at 113 schools (121 if you include iSAMS, their sister MIS), up from 105 (115 inc. iSAMS) the previous year. That's a significant slow-down in the annual rate of growth (8% increase in the past year vs 40% the year before). So while they're not exactly looking sickly, they still need to find The Cure for this year's relative stagnation to cement themselves as a viable alternative to the big 3.

6. I've got schools, they're multiplying.

In Spring 2023 I wrote about how Compass Education had achieved an eye-popping 300% term-on-term growth rate... by growing from 1 to 4 schools. Building on my past experience as a management consultant, I did some whizzy maths and projected that at this rate "in 2028 they will be working with over a billion schools." Well, you might have laughed at me then, but this year has seen them grow from 7 to 30 schools. That's a growth rate of over 300%, so I feel VINDICATED. Admittedly this is an annual rate whereas previously I was citing a termly metric, but still, I maintain that Compass's race to 1 billion is still on.

7. Papa's got a brand new bag.

Hoo boy, am I glad to see Satchel enter the MIS market! You can only imagine how much time I've wasted over the years trying to come up with puns for Arbor and Bromcom - but there's really just not much there to work with. Satchel, on the other hand, offer a whole world of bag-themed plays on words to explore.

And more importantly, if you're a MIS purchaser, they give you another intriguing alternative to build into your procurement process. A significant chunk of secondary schools already use Satchel One, the homework and learning platform, so the company has an inbuilt advantage when launching their MIS product, in that they already have a commercial relationship many prospective customers. I'll be intrigued to see how their market share evolves in the coming years.

One other mildly interesting thing to note about Satchel is that they originally burst onto the UK scene under the Show My Homework brand. Their pitch as I remember it was that they DIDN'T have lots of modules, unlike the sprawling and clunky incumbent learning platforms of the day. They did one thing, but they did it jolly well. Over time that strategy evolved as they became Satchel, a platform combining lots of modules. Now, they're having a crack at competing in the broadest edtech category out there: a full MIS! I think their story tells you quite a lot about how edtech has evolved over the past decade. There was a time when it was ok to be a narrow product doing one thing well, but increasingly, customers, management teams and investors are backing fewer, broader vendors to do a range of things for them.

8. I'm still standing.

It's not been an easy few years for Juniper in the MIS market. They acquired Pupil Asset in 2020, and then launched a new MIS called Horizons in 2022. The combined Pupil Asset+Horizons share of schools now stands at 284, down from 467 in 2021. However, they're very much still in the fight, having launched a brand new MIS called Juniper MIS this term. Come back next year to see how that product has fared in its first year on the market...

9. Ready to die.

... But when you do come back, you won't find me talking about Advanced Learning anymore. The company announced almost two years ago that they would go end of life by August 2023, so honestly, I was surprised it took until now for the last of their schools to disappear from the England state school dataset. But they are now gone, so I guess the last time I'll mention them. Let's have a minute's silence for their ill-starred products: Facility CMIS and Cloud School (formerly Progresso). CMIS in particular will be fondly remembered by some veteran data managers out there, who enjoyed building MacGyver-esque customisations on top of their flexible (if anachronistic) database. Still, it's fair to say that their days have been numbered for a while. There was once a time when it seemed like they would be a Biggie, but in the end they didn't even manage to sustain being Smalls.