After a few fun hours interrogating the data I reckon there are a few noteworthy insights - and you can play around with the stats for yourself using the Tableau Story below. As always, my thoughts are below the dataviz, so scroll down if you just want to know the headlines.

So, here's my take:

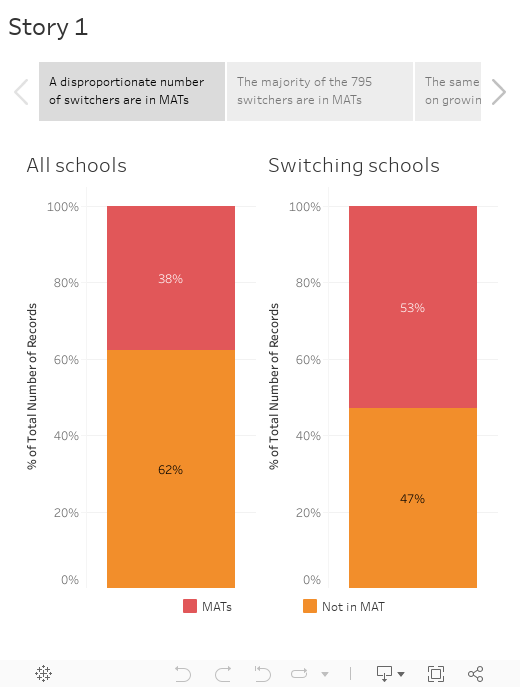

- The majority of switching schools are in MATs. 53% of switching schools were in MATs, whereas 38% of schools in the dataset are in MATs. Both figures are notably high and deserve scrutiny. With the former, it's clear that if you want to grow your market share, you need a MAT offer - even those MIS who are picking up standalone schools have a strong MAT presence too. In the case of the latter, with fully 38% of all schools reporting a census return being part of MATs, Trusts now represent over a third of the English MIS market. This is a big deal - anecdotally my experience is that people still think of MATs as more like a quarter of the market, or even less.

- Six vendors grew their market share. Once again the biggest winner is Scholarpack, who picked up 344 schools, making them the fastest grower in absolute terms for over two years now, and the clear third placed vendor overall (after SIMS and RM Integris) with over 1,000 schools. The next three largest climbers will all be pleased with progress: Pupil Asset netted 131; Arbor gained 102; and Bromcom added 67. RM will also presumably be happy to add 32, given they start with a solid 10% market share (keeping them as the clear second placed vendor after SIMS). And SchoolPod also added another 28, taking them over the psychologically important 100 school mark.

- 796 schools switched MIS in the past 12 months. That's close to the all-time high we saw in September 2017, when 860 schools switched. MIS investors, founders and senior leaders I speak to are bullish that the number is continuing to rise. So a 1,000+ switching dataset in autumn 2018 is a real possibliity.

- Regional strongholds are emerging for certain vendors. The map views on the above viz (tabs 5 and 6 on the Tableau Story) show that Pupil Asset is dominant in Norfolk, and growing nicely in a corridor stretching from there down to Cornwall. Arbor appear to have some promising concentrations in London, the North West and the South West. RM's three particularly strong clusters are the South & South East (from Oxfordshire to Southend), the East & North East (Peterborough to Doncaster) and the North West (Halesowen to Bradford). Bromcom have impressive take-up in London (anchored by MATs including Harris Federation and Ark Schools). And while Scholarpack have slightly broader coverage, the North West (Lancashire and Cumbria), the East (Nottingham and Lincolnshire), the West and West Midlands (Birmingham to Herefordshire), and London. On the other hand, iSAMS and Schoolpod have no significant discernible clusters.

- There's a new vendor in town! A warm welcome to Faronics Wise, who added their first English state school. This Canadian company claims 30,000 unique customers in 150+ countries, so it will be fascinating to track their investment in this new market for them.

A final note: as mentioned previously, in my day job I run Assembly, a schools data platform that has relationships with most of the companies mentioned above. For that reason, I stick to data-driven observations in these posts to help people interpret the data, and I don't personally express MIS preferences or offer recommendations.